Tracking Shareholder Proposals and Company Exclusions: Pre-Season Observations

Subscribe

Key Takeaways

- In November 2025, the SEC's Division of Corporation Finance announced it would no longer provide responses to most no-action requests to exclude shareholder proposals.

- Based on early incoming data, the number of shareholder proposals going to a vote in January and February 2026 is down from last year, while the number of exclusion notices filed is roughly the same.

- The absence of SEC no-action relief may have encouraged some companies to be more cautious about what proposals they exclude, and their basis for exclusion.

- Investors are pushing back on proposal exclusion via litigation – and getting results.

- Compared to 2025, more of the shareholder proposals that have gone to a vote cover environmental and social topics.

How has the SEC’s new approach to no-action requests1 impacted the shareholder proposal landscape? It’s a question that Glass Lewis will be monitoring throughout the U.S. proxy season.

With proxy season only just beginning, it’s too early to draw any firm conclusions -- but not too early to look at the data. In the first instalment of an ongoing series on shareholder proposals and company exclusions, we share what we’ve observed in January and February, and offer some early insights.

Proposal and Exclusion Request Volumes

Key Takeaway #1: The number of shareholder proposals going to a vote in January and February is down from last year, while the number of exclusion notices filed is roughly the same.

Before looking at the data, it’s important to note that this represents a tiny sample size, making up less than 1% of the 4000+ U.S. meetings that Glass Lewis will cover this proxy season. While certain companies tend to attract shareholder proposals year after year, there’s always fluctuation.

Figure 1. Number of Shareholder Proposals and Exclusion Notices at January and February Shareholder Meetings

Source: Glass Lewis Research with no-action requests compiled from SEC.2 Note: Data is for proposals and notices relating to shareholder meetings held Jan. 1 - Feb. 28. Excludes withdrawn exclusion notices, and (for 2026 data) notices filed prior to November 17, 2025.

While the decline in the number of shareholder proposals is notable, it may not be directly related to the shift in how the SEC approaches exclusions. Among the 11 companies with a January or February meeting date that had a shareholder proposal on their ballot in 2025 but not in 2026, only one has filed to exclude a proposal from this year’s meeting.

Rather than representing a new phenomenon, the decline in the number of shareholder proposals going to a vote aligns with an ongoing, multi-year trend driven by other factors3 — including a prior change in SEC guidance that narrowed the scope for environmental and social proposals, growing pushback on ESG, and the widespread success of prior shareholder proposals in addressing investor concerns on many of the topics that have been the subject of recent activism.

Let’s take a closer look at the four companies that saw the most shareholder proposals in January and February of last year. Overall, this group has three fewer shareholder proposals on their agendas in 2026 (down from 14 to 11), and is only excluding one proposal (down from five last year).

- Apple is down from four shareholder proposals in 2025 to one in 2026, and its use of the no-action mechanism is down as well: they excluded three proposals last year, and one this year.

- Deere is down from five shareholder proposals to three, with zero exclusion notices after filing two last year.

- Tyson Foods is up from one shareholder proposal to three, and did not file exclusion notices in either year.

- Visa has had four shareholder proposals on its ballot in each year, and did not file exclusion notices in either year.4

How Companies Are Leveraging Proposal Exclusion

Key Takeaway #2: The absence of SEC no-action relief may encourage some companies to be more cautious about what proposals they exclude, and their basis for exclusion.

While the SEC’s change can be interpreted as giving boards free rein to set their meeting agendas, some companies appear to be taking a more cautious approach. A number of companies that filed exclusion notices prior to the November 17 announcement (Analog Devices, Apple, Costco, Starbucks and Tyson Foods) did not receive any response from the SEC, did not withdraw or refile their notices, and ultimately allowed these shareholder proposals go to a vote. It seems reasonable to speculate that the absence of no-action relief, and resulting increased potential for shareholder opposition or even litigation, was a significant factor in these decisions. Each of these notices sought to exclude the proposal on a substantive — and in effect subjective — basis.5

The SEC’s new approach could also have an impact on the grounds companies cite to exclude proposals. While to date companies have continued to cite a range of different bases for their exclusion requests, we may see more reliance on procedural reasons under the new regime. Three of the seven total requests filed for January and February 2026 meetings relied solely on a technical basis for exclusion. By comparison, five of the eight total notices filed for 2025 meetings in the same period cited a technical basis for exclusion.

Notably, one of the other four notices filed for January and February 2026 meetings focuses on the technical basis for exclusion, while also noting (but not substantiating) the company’s belief “that there also are substantive bases” for excluding the proposal. The decision to focus solely on more clear-cut procedural issues could indicate that, absent cover from SEC staff, companies may be looking to avoid relying on substantive reasons, which can be open to debate.

Investor Responses to Proposal Exclusions: Litigation and Campaigns

Key Takeaway #3: Proponents are pushing back on exclusion notices.

The absence of SEC no-action relief leaves boards exposed. In our engagement discussions, we’ve heard that companies are more willing to negotiate around shareholder proposal exclusions. Where negotiations fail, lawsuits at AT&T, Axon Enterprises and PepsiCo have already been effective in pushing back on those companies’ attempts to exclude shareholder proposals.

- AT&T reached a settlement with the proponent, a group of New York City pension funds,6 allowing a resolution on workforce diversity disclosure to go to a vote after excluding it on the basis that it covered ordinary business.

- Similarly, PepsiCo reached a settlement with PETA after initially excluding a proposal requesting reporting on the treatment of animals in company and partner supply chains on procedural grounds.7

- A judge ordered Axon Enterprises to work with the Nathan Cummings Foundation to find a compromise,8 after the proponent sued the company over its decision to omit a request for political contributions reporting on the basis that it micromanaged the company.

More lawsuits are being filed. Most recently, New York State’s comptroller sued BJ’s Wholesale Club Holdings after the company excluded a proposal seeking a deforestation risk assessment, and As You Sow sued Chubb over a request for reporting about subrogation of climate-related losses. Both proposals have been excluded on the basis that they interfered with ordinary business.9

In addition to lawsuits, vote-no campaigns represent a potential avenue for escalation. Investors’ ability to communicate these campaigns, however, could be hampered by another recent SEC change, Typically, investors will file exempt solicitations on the SEC’s website as a means to express concerns and provide details concerning their recommendations in support of or against resolutions brought to a shareholder vote, including to advance vote-no campaigns. Earlier this year, the SEC announced it would object to the filing of exempt solicitations by investors who hold less than $5 million in company shares. Because many of the groups and individuals that frequently utilize this process are smaller shareholders, this could place some constraints on investors’ use of this communication tool.

Proposals Still Making It Onto the Ballot

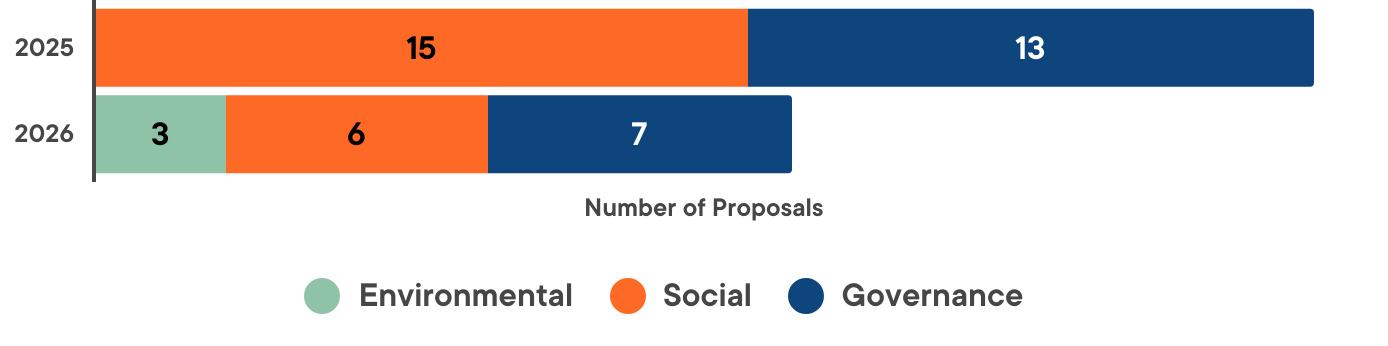

Key Takeway #4: Compared to 2025, a larger proportion of shareholder proposals that have gone to a vote cover environmental and social topics.

The (limited) reemergence of environmental proposals so far in 2026 (Figure 2) might come as a surprise after several years of declining numbers.

Figure 2. Breakdown of January and February Shareholder Proposals by Topic

Source: Glass Lewis Research. Note: Data is for proposals relating to shareholder meetings held Jan. 1 - Feb. 28.

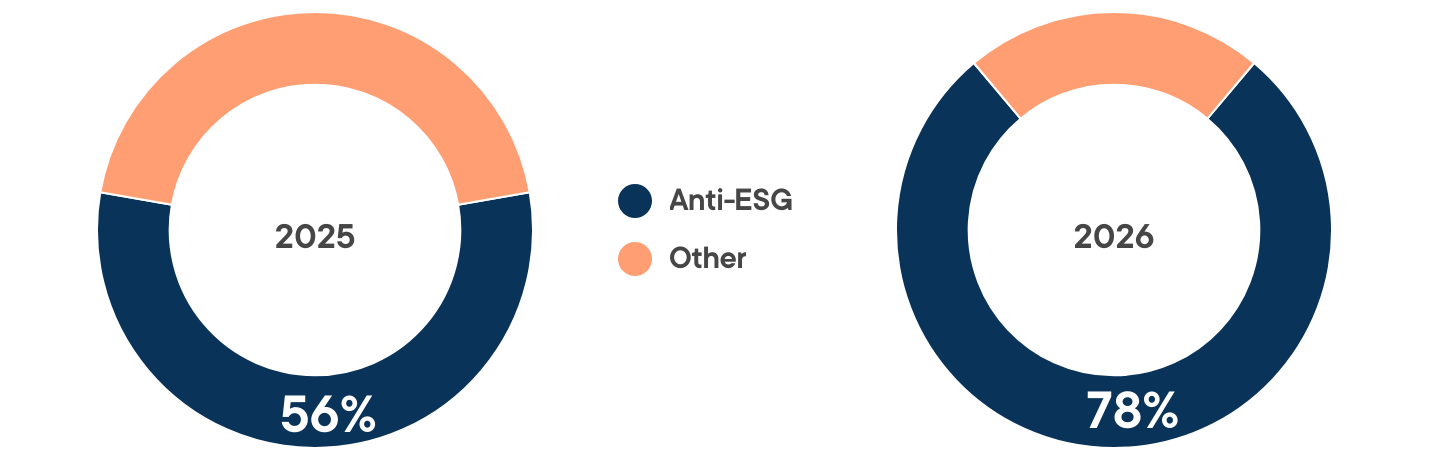

However, this appears to be driven by the growth in so-called “anti-ESG” activism. Notably, the proportion of E&S proposals at 2026 meetings to date that have been submitted by anti-ESG proponents is up compared to the same period in 2025, and represents an overwhelming majority of total E&S proposals (Figure 3).

Figure 3. Proportion of January and February E&S Proposals Submitted by Anti-ESG Proponents

Source: Glass Lewis Research. Note: Data is for proposals relating to shareholder meetings held Jan. 1 - Feb. 28.

The decline in the proportion of governance-related proposals, shown in Figure 2 above, may partly reflect companies improving their governance practices.

For example, two of the governance-related shareholder proposals that went to a vote in January/February 2025 requested the adoption of a simple majority vote standard, compared to none so far in 2026. Both of those 2025 proposals were supported by a majority of shareholders, and the board of Post Holdings responded by engaging with investors and submitting proposals to remove most supermajority vote requirements. Further, a simple majority proposal was submitted for Skyworks Solutions’ 2026 AGM, but it was excluded by the company on the basis that it had already been substantially implemented.

What Does This Mean?

It’s still too early to say definitively, but the impact of the new exclusion regime does not appear to be definitive. Shareholder proposals are still being submitted, and still going to vote, as investors, proponents and companies navigate the new landscape.

- For investors: How boards respond to shareholder proposals in the wake of the SEC shift adds another component to assessing governance practices and director performance.

- For proponents: In the first year, with market expectations still forming and individual company approaches widely diverging, proponents will have to be prepared for either business as usual or outright rejection, while also exploring their options to escalate.

- For companies: Conversely, companies that do file exclusion notices will need to be prepared for a range of responses from proponents, up to and including litigation.

- For all parties: The uncertainty of the current environment highlights the importance of engagement and dialog.

With thousands of meetings still to come, and more exclusion notices being filed every week, Glass Lewis will continue to monitor this topic and share our findings.

Notes and References

1 U.S. Securities and Exchange Commission. Division of Corporate Finance. "Statement Regarding the Division of Corporation Finance's Role in the Exchange Act Rule 14a-8 Process for the Current Proxy Season." November 17, 2025. https://www.sec.gov/newsroom/speeches-statements/statement-regarding-division-corporation-finances-role-exchange-act-rule-14a-8-process-current-proxy-season

2 U.S. Securities and Exchange Commission. “2025-2026 Correspondence Under Exchange Act Rule 14a-8.” Accessed March 5, 2026. https://www.sec.gov/rules-regulations/shareholder-proposals/2025-2026-responses-issued-under-exchange-act-rule-14a-8

3 Keatinge, Courteney. “The Evolving Investor Approach to Climate: Examining Shareholder Proposals as a Forum on Climate Change, Reporting and Emissions.” Glass Lewis. December 18, 2025. https://www.glasslewis.com/article/the-evolving-investor-approach-to-climate-examining-shareholder-proposals-as-a-forum-on-climate-change-reporting-and-emissions

4 Visa filed its proxy in early December, shortly after the SEC announcement, so may not have had sufficient time to avail itself of the new process.

5 In excluding proposals, companies must cite a basis for exclusion. These bases can be categorized as either technical/procedural (for example, that the proponent failed to provide proof of ownership, or that proposals were submitted after the deadline) or substantive (for example, that the proposal request would interfere with the company's ordinary business, or has already been substantially implemented). Whereas technical objections are typically clear cut (the proposal was either submitted on time, or it wasn't), in many cases substantive objections are subjective, and open to debate.

6 NYC Comptroller. “NYC Pension Funds and AT&T Reach Settlement for Unlawful Exclusion of Shareholder Proposal Requesting Workforce Demographic Data Disclosure.” February 26, 2026. https://comptroller.nyc.gov/newsroom/nyc-pension-funds-and-att-reach-settlement-for-unlawful-exclusion-of-shareholder-proposal-requesting-workforce-demographic-data-disclosure/

7 PeTA. “Victory! PepsiCo to Allow Shareholder Vote on Bull-Abuse Concerns After Lawsuit.” February 24, 2026. https://www.peta.org/media/news-releases/victory-pepsico-to-allow-shareholder-vote-on-bull-abuse-concerns-after-lawsuit/

8 Gambetta, Gina. “Judge orders Axon to work with investor on “compromise” shareholder proposal.” Responsible Investor. March 3, 2026. https://www.responsible-investor.com/judge-orders-axon-to-work-with-investor-on-compromise-shareholder-proposal/

9 Gambetta, Gina and Webb, Dominic. “New York State Comptroller, As You Sow Add to Lawsuits Over Shareholder Proposals.” Responsible Investor. March 4, 2026. https://www.responsible-investor.com/new-york-state-comptroller-as-you-sow-add-to-lawsuits-over-shareholder-proposals/