The Evolving Investor Approach to Climate: Examining Shareholder Proposals as a Forum on Climate Change, Reporting and Emissions

Subscribe

Key Takeaways

- In the 2025 proxy season, climate-related proposals made up over three-quarters of all environmental shareholder proposals. However, no climate-related proposals – or environmental proposals more broadly – received majority shareholder approval.

- Despite a lower number of climate-related shareholder proposals going to a vote, the 2025 proxy season saw a slight increase in the number of climate reporting proposals. But voting support has continued to decrease.

- Average support for proposals on emissions reductions targets dropped by more than half this year, to 12%. Unlike previous years, none of these proposals received majority shareholder support.

- Whereas average support remained static for shareholder proposals as a whole at 23%, it was cut in half for climate-related shareholder proposals, from 22% last year down to 11% in 2025.

Investors’ consideration of climate and other environmental, social and governance (ESG) matters has evolved significantly in recent years. In the last decade, ESG has gone from a niche topic within stewardship, largely addressed via shareholder proposals, to a mainstay in the routine evaluation performed by mainstream investment managers.

Yet as core elements of climate reporting and oversight have become embedded in governance practices and investment decisions, voting support – that is, for the shareholder proposals that were historically a key mechanism for U.S. climate stewardship – has been declining. The decline stems from a number of potential factors, in part from the influence of the anti-ESG movement and an emerging geographical divergence in how shareholders and companies view these topics; and in part from a shift in the types of ESG proposals going to a vote, now that best practices for many aspects of climate governance and reporting have been established and widely implemented.

From the standpoint of the 2025 proxy season, this article looks at the volume and support for shareholder proposals on climate change, climate reporting and emissions reductions, and discusses how these trends have been impacted by shifts in the broader stewardship landscape.

Climate Change Proposals and Declining Majority Support

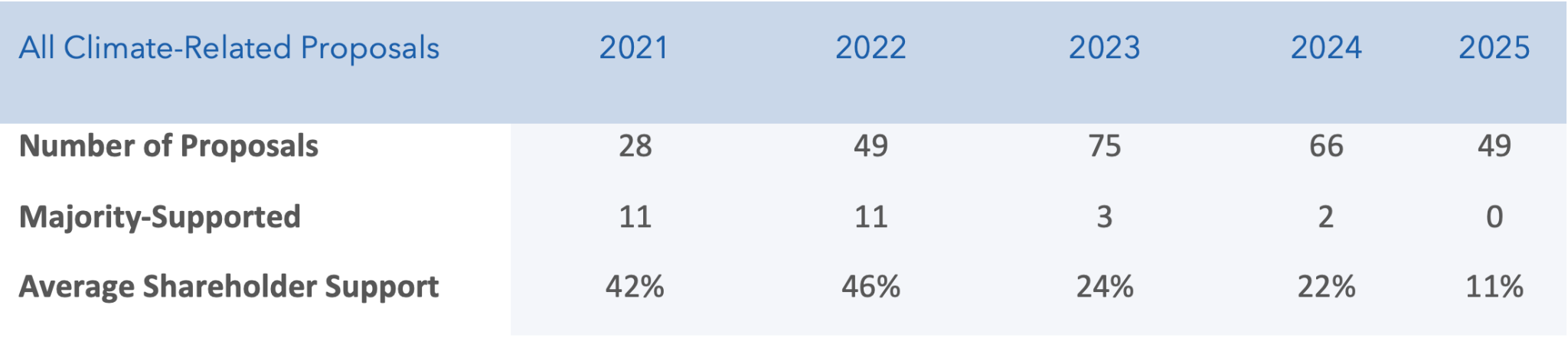

Over the last decade, the number of and investors’ focus on shareholder proposals concerning climate-related issues has grown significantly. This includes requests for additional disclosures and actions as it relates to companies’ contributions to and impacts on climate change. Moreover, given the wide-reaching impacts of climate change, most environmental proposals have addressed climate-related topics in recent years. In fact, in 2025, climate-related proposals made up over three-quarters of all environmental proposals.

Although the number of these proposals has grown, support for these initiatives has been slowly declining in recent years. Prior to 2017, no climate change-related shareholder proposal had ever received majority support. But that year, three such proposals received over 50% approval. Since then, an additional 15 proposals, including two in 2024, have received majority shareholder support. However, in 2025, no climate-related proposals, or environmental proposals more broadly, received majority shareholder approval (Table 1).

Table 1. Summary of Climate Change Proposals, 2021-2025

Source: Glass Lewis Research. Note: Data as of 2025 proxy season period from Jan. 1 to June 30, 2025.

Despite the lack of majority support for any of these proposals in 2025, the consistently high number of proposals on climate-related issues and the support garnered for them is likely indicative of shareholders’ growing realization that issues related to climate change pose significant risks to investors and the companies in which they invest.

Higher Volume, But Diminishing Support on Climate Reporting Proposals

In light of growing shareholder interest and understanding on the part of companies that climate change could present significant risks to their operations, there has been a significant uptick in corporate reporting on climate impacts and risks. In theory, the trend has negated the necessity of submitting shareholder proposals on this topic. In reality, however, the dynamic nature of climate change and shareholders’ increasing sophistication on this issue has resulted in more detailed and company-specific requests related to climate reporting.

Despite a lower number of total shareholder proposals going to a vote, including those related to climate issues, this year saw an increase in climate reporting proposals (see Table 2 below). In line with other types of proposals, support has continued to decrease. The lower levels of support could be due in part to the anti-ESG movement and a greater reluctance from shareholders to support environmental and social shareholder proposals, and in part to the composition of the proposals that went to a vote. Unlike several years ago, when most climate proposals had similar requests, in the last four years, there were nearly as many distinct requests as there were proposals.

Table 2. Summary of Climate Reporting Proposals, 2021 - 2025

Source: Glass Lewis Research. Note: Data as of 2025 proxy season period from Jan. 1 to June 30, 2025.

Several of these proposals asked for specific accounting of certain types of emissions. For example, a proposal at Markel Group requested that the company disclose the emissions from its “underwriting, insuring, and investment activities that account for major sources of its GHG footprint.”1 In addition, a proposal at Skyworks Solutions requested the disclosure of all material Scope 3 greenhouse gas (GHG) emissions.2 Other proposals dealt with companies’ operational strategies, such as a proposal at The Travelers Companies that requested disclosure on the expected impact of climate-related pricing and coverage decisions on the sustainability of its homeowners insurance customer base under a range of climate scenarios in the near, medium, and long-term. Another proposal, submitted at The Southern Company requested disclosure on the utility’s decision to increase reliance on fossil fuel-based energy production rather than renewables.3 All of these proposals received between 7% and 21% support.

Lower Number and Support for Emissions Reduction Targets Proposals

For many years, shareholders have proposed resolutions requesting that companies adopt GHG reduction targets. Particularly given the increased focus on issues related to the environment and climate change, it is unsurprising that shareholders are continuing to press companies to take steps to minimize their environmental impacts. However, over the last decade there has been a shift in how shareholders are approaching this issue, the number of proposals going to a vote, and where these proposals are submitted.

From 2019 through 2021, we reviewed ten of these proposals in total. However, when the SEC changed its criteria for allowing no-action requests in 2022, proposals asking companies to establish GHG reduction targets became more commonplace.

Historically, emissions reduction proposals had called for companies to develop their own targets and focused on issues like Scope 1 and Scope 2 emissions, which are under management control with a relatively widely-accepted link to shareholder value for companies in relevant industries. But with Scope 1 and 2 emissions targets now common across the market, the proposals going to a vote increasingly cover topics where there is far less market consensus regarding the link to shareholder value, like downstream Scope 3 emissions that are beyond management's control; or calls for companies that have already taken steps to go even further. In some cases, these proposals prescribe specific goals or outcomes, which many asset managers believe should be left to management and the board.

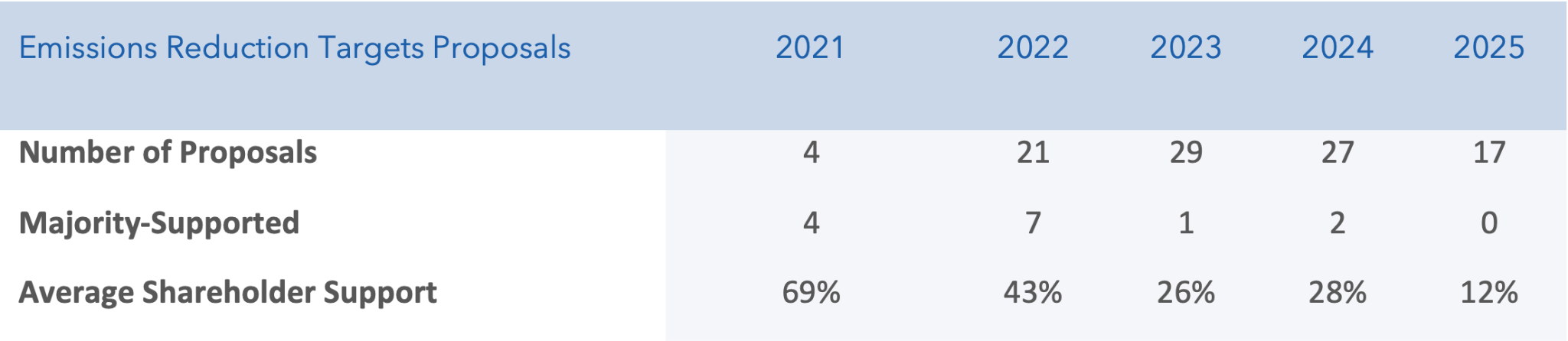

The increase in proposal volumes has also been influenced by a wider base of companies where these proposals were submitted. Initially, these proposals were submitted almost exclusively at companies operating in the oil and gas industry or in heavily emitting industries, such as utilities. In the last several years, proponents have submitted proposals at companies that are less emissions-intensive. In 2025, only two of the 17 proposals on this topic were at companies where GHG emissions presented a material risk to the target companies, down from 33% and 41% and 33% in 2023 and 2024, respectively. Further, one of these two ‘material’ proposals, submitted at ConocoPhillips, requested the elimination of the oil and gas company’s GHG reduction targets (the only proposal of its kind in 2025).

Table 3. Summary of Emissions Reduction Targets Proposals, 2021-2025

Source: Glass Lewis Research. Note: Data as of 2025 proxy season period from Jan. 1 to June 30, 2025.

In 2025, average support for these proposals dropped by more than half, to 12% (Table 1 above). Moreover, unlike previous years, none of these proposals received majority shareholder support.4 In the last year, the highest support for one of these proposals (30.4%) was at BJ’s Wholesale Club Holdings. Fewer than half of these proposals received over 10% support. This is a stark departure from 2024 when average support was 28% and two of these proposals received majority shareholder support, with a third proposal receiving 49.9%.

The Broader Context for Lower Voting Support

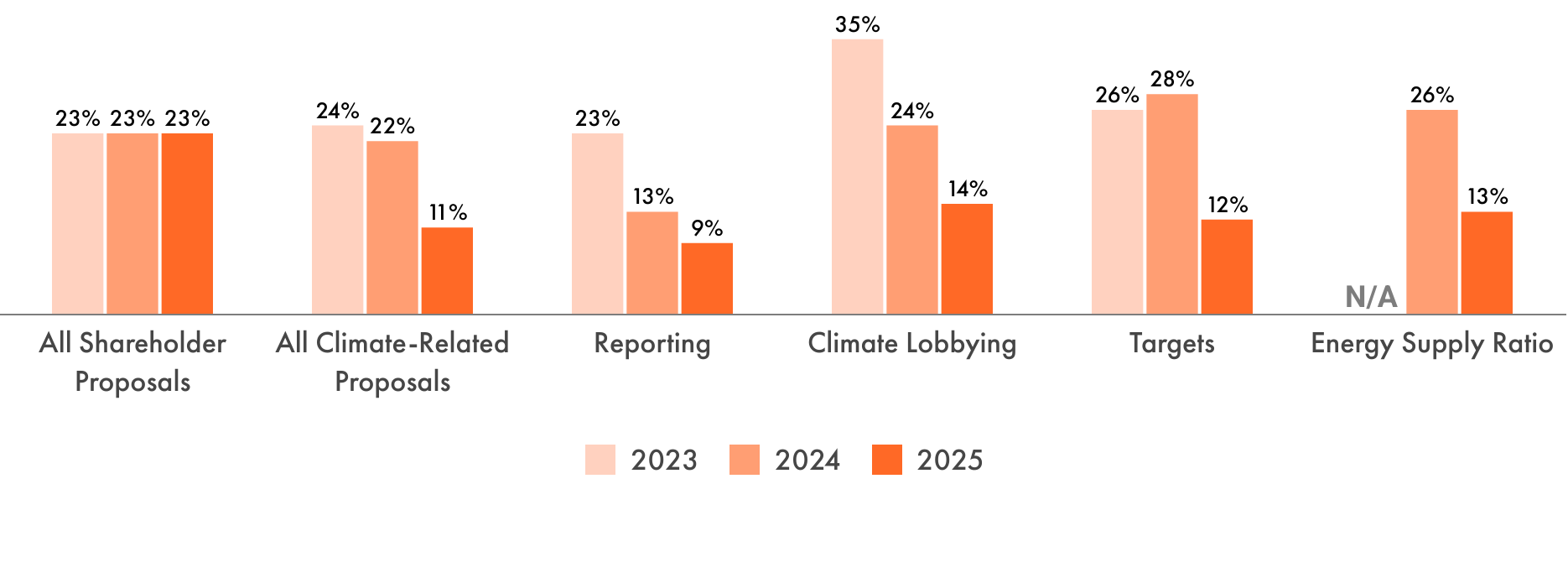

Over the past three years, average shareholder support for climate-related shareholder proposals has declined across every sub-category, and by more than 50% overall. Meanwhile, average shareholder support for all shareholder proposals has remained static at 23% over this period (Figure 1).

Figure 1. Average Shareholder Support for Climate-Related Shareholder Proposals

Source: Glass Lewis Research. Note: Data as of 2025 proxy season period from Jan. 1 to June 30, 2025.

A Shifting Landscape: Anti-ESG and Regional Bifurcation

One potential factor influencing the decline in voting support for climate proposals is the anti-ESG movement, which has put a damper on how many companies and investors are openly discussing and addressing environmental issues. Some of this has been experienced only in certain markets and has resulted in a growing bifurcation of how market participants are integrating these considerations in their operational and investment decisions.

For example, many companies and investors in Europe have strengthened their ESG considerations in the last several years, driven, in part by regulations and social expectations. By contrast, many U.S. companies and investors have eliminated or scaled back many of their ESG-related initiatives, particularly those related to climate.5 Our 2025 Policy Survey found a significant geographic split between U.S. investors and those from other regions, on how they approach environmental stewardship topics like climate transition plans and biodiversity.6

Proposal Requests and Investor Expectations

However, that’s not the only factor at play. The decline in voting support on climate likely stems in part from the very success of prior shareholder proposals, and stewardship efforts more broadly. In response, U.S. companies have been producing increasingly robust sustainability reporting, thus addressing much of the low-hanging fruit that was previously addressed via the shareholder proposal process. As the integration of best practices for climate disclosure and oversight has spread across the market, shareholder proposals have shifted to more prescriptive requests. For example, proposals requesting that companies produce sustainability reports were common and often received strong support. However, given the vast majority of companies now provide such reports,7 many proposals are now instead requesting highly-specific reporting that, in many instances, is already covered in some form by companies’ existing reporting.

At the same time, many asset managers have become increasingly knowledgeable about environmental issues and their financial implications, expanding the scope of their ESG stewardship beyond shareholder proposals to integrate climate considerations within their engagement programs, board evaluations, and broader investment criteria. They have also become more discerning in their proxy voting – more likely to go beyond shareholder proposals and vote against director elections or compensation proposals based on climate concerns. But they are also less willing to support proposals they do not view as well-crafted or addressing financially material issues, regardless of their general views on the topic raised by the proposal.

Conclusion

Climate remains a key issue for many investors around the globe – but one that is increasingly viewed in the context of financial materiality, and where the process of establishing general standards and expectations has developed to a more mature stage. With shareholders incorporating nuanced, company-specific climate considerations into their engagement program, assessment of board performance and broader investment criteria, climate stewardship has expanded beyond the traditional forum of shareholder proposals.

Notes and References

1 Markel Group. 2025. Notice of Proxy Statement for 2025 Annual Meeting. Accessed October 24, 2025. https://proxy.mklgroup.com/materials/2025/Markel%20Group%20Inc.%20-%20Notice%20and%20Proxy%20Statement%20for%202025%20Annual%20Meeting.pdf

2 Skyworks. 2025. Notice of 2025 Annual Meeting and Proxy Statement. Accessed October 24, 2025. https://www.skyworksinc.com/-/media/SkyWorks/Documents/IR/2024-SWKS-Annual-Report.pdf

3 Southern Company. 2025. Notice of Annual Meeting of Stockholders & Proxy Statement. Accessed October 24, 2025. https://www.southerncompanyannualmeeting.com/media/vbshsrga/438571-1-_40_southern-company_nps_wr.pdf

4 Overall voting support and number of proposals submitted for all shareholder proposals in 2025 is covered in greater detail in Glass Lewis. 2025. Shareholder Proposals: Proxy Season Review 2025.

5 Glass Lewis. Shareholder Proposals: Proxy Season Review 2025. Page 5.

6 Glass Lewis. 2025. “Policy Survey Shows a Shifting Stewardship Landscape, and Diverging Investor Views Across Regions” Accessed October 24, 2025. https://www.glasslewis.com/article/policy-survey-shows-a-shifting-stewardship-landscape-and-diverging-investor-views-across-regions

7 Glass Lewis. 2025. In-Depth Report: Sustainability Reporting. Accessed October 24, 2025. https://grow.glasslewis.com/sustainability-reporting

.jpg)