Policy Survey Shows a Shifting Stewardship Landscape, and Diverging Investor Views Across Regions

Subscribe

Key Takeaways

- 85 percent of investors and 76 percent of non-investors say they do not base governance votes solely on financial performance.

- With Texas and Nevada amending their laws to attract more companies, 50 percent of investors are focusing more on shareholder rights when assessing reincorporation.

- 44 percent of U.S. investors view the CEO-to-median-employee pay ratio as “not important”, compared to just 8 percent of non-U.S. investors.

- U.S. based investors are far more likely to ignore diversity factors in their evaluation of boards (42%) compared to investors from other regions (6%).

Glass Lewis’ annual policy survey provides investors, corporate issuers and other market participants with the opportunity to weigh in on policy areas where we have recently observed new practices, or where our previous discussions and engagements discussions have not yielded a clear consensus.

This year’s survey covers many of the corporate governance topics currently making headlines, revealing notable shifts and ongoing divides between investor and non-investor views, along with some emerging areas of consensus. It also illustrated some significant geographic gaps between investors from the U.S. and other regions on their approach to a range of topics that are central to stewardship and proxy voting. In total, Glass Lewis received 76 responses from investors and 310 responses from non-investors.

This article provides an overview of some of the most notable findings, including topics that have been at the center of the recent governance, stewardship and regulatory conversation, and examples of regional differences among investors.

Shifting Stewardship Landscape: Recent Headlines & Developments

Basing Governance Votes on Financial Performance

A significant majority of both investors (85%, including all participating asset managers) and non-investors (76%) firmly rejected the notion of basing voting decisions for director elections, bylaw amendments and other governance-centric proposals solely on financial factors.

U.S. investors were more likely to respond “Yes” or “Yes, in certain circumstances” (16%) compared to investors from other regions (5%), with all of these representing state public sector pensions.

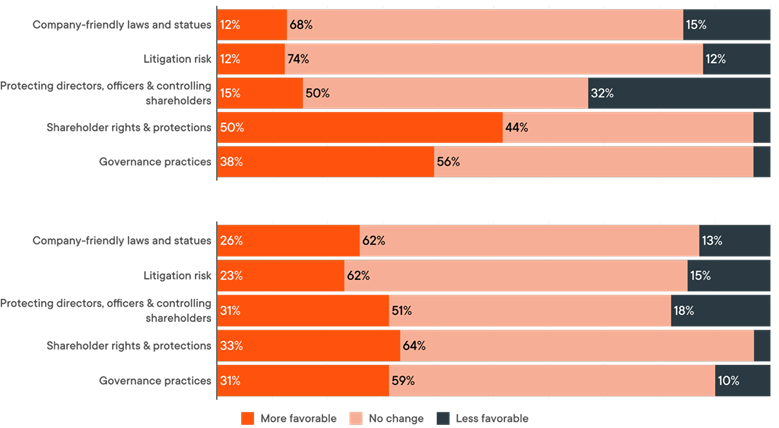

Reincorporation

Over the past year, many U.S. states have amended their corporate laws to attract or retain companies. Changes include establishing specialized business courts, providing increased protection for directors, officers, and controlling shareholders, reducing litigation risk, and providing greater clarity on the standards for director independence and/or disinterestedness.

In response to this shifting landscape, half of investors reported that they are putting more emphasis on shareholder rights and protections (compared to just one-third of non-investors. Conversely, compared to investors, non-investors were over twice as likely to have become more favorable to company-friendly laws and statutes, litigation risk, and protecting directors, officers and controlling shareholders.

In light of recent developments, have you changed your approach to any of these considerations when evaluating reincorporations?

Make Whole Awards

Over the past year, use of the make-whole designation for U.S. sign-on awards has risen. Over half of all S&P 500 sign-on awards were identified as make-whole compensation this year, compared to 38% in 2024.

Non-investors were far more likely to view make whole awards as fundamentally different from other sign-on awards (40.8%, compared to just 5.3% among investors). Investors were split; while the top answer was to treat make whole grants on the same basis as other sign on awards (50%, compared to 27.6% among non-investors)), nearly as many were willing to view them differently so long as the grants are fully disclosed and clearly equivalent to what was forfeited (44.7%, compared to 31.6% among non-investors).

Ownership Thresholds for Shareholder Actions

Certain states have recently adopted increased ownership limitations for shareholders to submit shareholder proposals or file derivative actions (e.g. 3% ownership for at least 6 months), limiting smaller shareholders’ ability to shape the company’s agenda.

There appears to be a significant gap between investor and non-investor views on the adoption of these increased ownership thresholds without shareholder approval. Whereas a majority of investors found this concerning, with 49% stating that directors should be held accountable when they stand for re-election, 82% of non-investors did not find the practice to be concerning.

Do you consider the adoption without shareholder approval of increased ownership thresholds for shareholders to submit proposals or file derivative actions to be concerning?

A Transatlantic Stewardship Gap?

Across a variety of topics and questions, we found significant gaps in the views and approaches of U.S.-based investors compared to investors in other regions. While some of these gaps were expected, for example on environmental and social issues, or likely reflected differing levels of familiarity with specific practices, others appeared to reflect broader underlying differences in corporate governance and stewardship expectations.

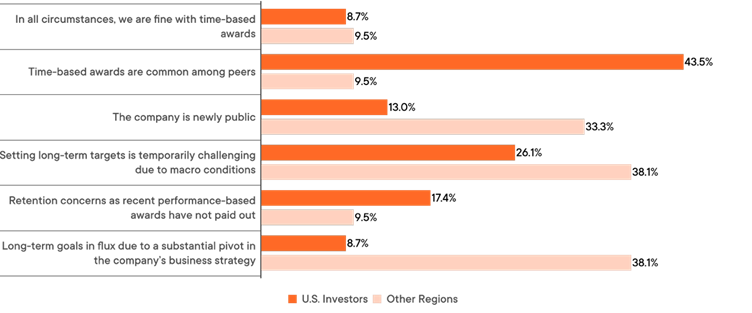

Time-Based Awards

U.S-based investors were far more open to the sole use of time-based awards as a part of the ongoing compensation structure so long as the practice was common with peers (43.5%, compared to 9.5% among investors from other regions) or as a retention measure (17.4% vs 9.5%). Meanwhile, investors from other regions appeared more likely to view them as a temporary stopgap, such was when the company is newly public (33.3%, compared to 13% among U.S. investors) or following a significant change in business strategy (38.1% vs 8.7%).

In what specific circumstances would you consider use of only time-based awards under a long-term incentive plan reasonable?

CEO Pay Ratio

To prepare for the possibility of reduced disclosures from the SEC regarding executive compensation, we asked for feedback on what elements of reporting are considered important to communicating and assessing U.S. executive compensation programs.

While most investor views were roughly aligned, there was a geographic split on the pay ratio, with 44% of U.S. respondents viewing it as not important, compared to just 8% among investors from other regions.

Board Diversity

U.S. based investors were far more likely to report ignoring diversity factors in their evaluation of boards (42%) compared to investors from other regions (6%). When we asked what diversity-related reporting they expected, U.S.-based respondents put more emphasis on the board’s overall approach to the topic (100% of U.S. investors, compared to 64.7% for non-U.S.), whereas investors from other regions were more likely to expect disclosure on board racial/ethnic disclosure (47.1% vs 23.5% among U.S. investors) and the presence of a “Rooney Rule” (52.9% vs 17.6%).

Say on Climate

Whereas non-U.S. investors take a strong interest in Say on Climate, U.S. investors (including those who are active on ESG issues) were more likely to reject these votes and treat climate stewardship as an engagement or board oversight issue. This was reflected on a question asking participants to rate the importance of various disclosures in assessing Say on Climate votes, with a consistently smaller proportion of U.S. investors viewing each disclosure as important, and more directly in the comments. For example, one U.S. asset manager stated that:

“We generally vote against say on climate proposals, as vote result is difficult to interpret and less decision-useful than other avenues available (such as engagement)”

Biodiversity

Three-quarters of non-U.S. investors are currently incorporating biodiversity into their stewardship program or plan to soon, and only 5% have no plans to. By contrast, only 8% of U.S. investors are looking into how to incorporate it, and 61% have no plans to do so.

Willingness to Defer to Board Decisions

Several of the survey questions asked investors about their approach to specific situations, including what actions they expected the board to take on issues ranging from pay outcomes to meeting format. Across a variety of topics, U.S. investors were consistently more likely to support the board’s approach, whereas non-U.S. investors were more likely to expect directors to explain and justify their decisions.

About the Glass Lewis Policy Survey

The Policy Survey should be understood in the context of Glass Lewis’ approach to proxy research, which serves a global client base with a broad range of views on corporate governance issues.

We do not employ (nor does this survey seek to establish) one-size-fits-all rules for proxy voting. Instead, our approach combines broad initial filters, used to identify outliers based on market best practices and investor expectations, with a deeper level of nuanced, case-by-case analysis that reflects each company’s unique circumstances.

For more information on our approach to proxy research, please contact us or see Glass Lewis’ library of Benchmark and Thematic Policy Guidelines, available on our website.

Looking for More?

Read the full Policy Survey 2025: Results & Key Findings report.