Key Takeaways

- The number of shareholder proposals at Japanese companies in proxy season 2025 was up 11% from 2024, reflecting a strong current of shareholder activism.

- The number of proposals focused on governance, compensation, board elections and dividends all increased from 2024 to 2025, while the number of environmental and social proposals dropped significantly.

- Several companies received proposals calling for increased shareholder input on dividend distribution, which had historically been under the board’s control, with one at Eiken Chemical receiving majority approval.

- Director elections at Fuji Media were contested in the wake of a third-party investigative report that exposed governance failures and sexual misconduct allegations.

- A “vote no” campaign from Taiyo’s second largest shareholder contributed to the failure to secure majority support for the reappointment of the company’s representative director, president, and CEO.

Shareholder proposals and other forms of activism are becoming more common in Japan,1 fuelled by growing scrutiny of public company governance practices and capital efficiency. During the 2025 proxy season, the number of shareholder proposals increased, but with fewer proposals on environmental and social topics and a stronger focus on governance, including board elections and compensation, as well as dividend policies. In addition, activists are moving beyond the traditional realm of shareholder proposals to directly contest board elections and conduct “vote no” campaigns.

This article illustrates recent shareholder activism trends in Japan with three examples of notable meetings where investors influenced the AGM agenda in 2025.

Shareholder Proposal Trends in Japan

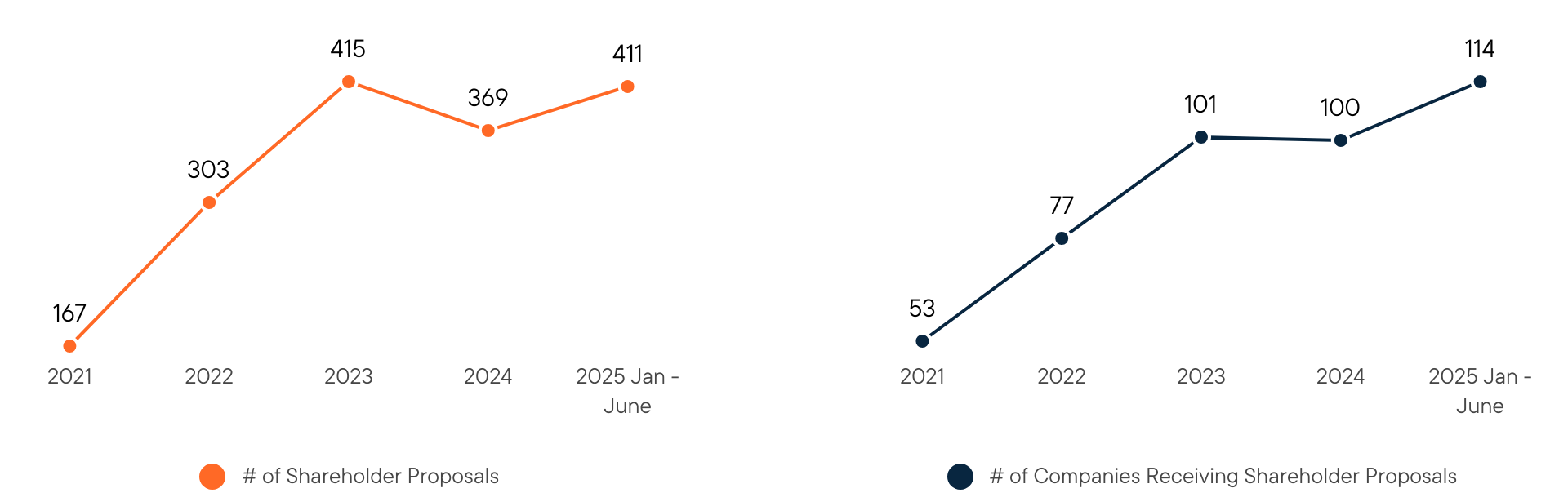

Increased investor activism in the Japanese market over the past five years has prompted a significant rise in the number of shareholder proposals, and in the number of companies receiving shareholder proposals. In the first half of 2025, both figures increased from the prior year, with 114 companies under Glass Lewis coverage receiving a total of 411 shareholder proposals.2

Figure 1. Number of Shareholder Proposals by Year

Source: Glass Lewis Research. Note: Data as of Jan. 1 to June 30, 2025 for the 2025 proxy season.

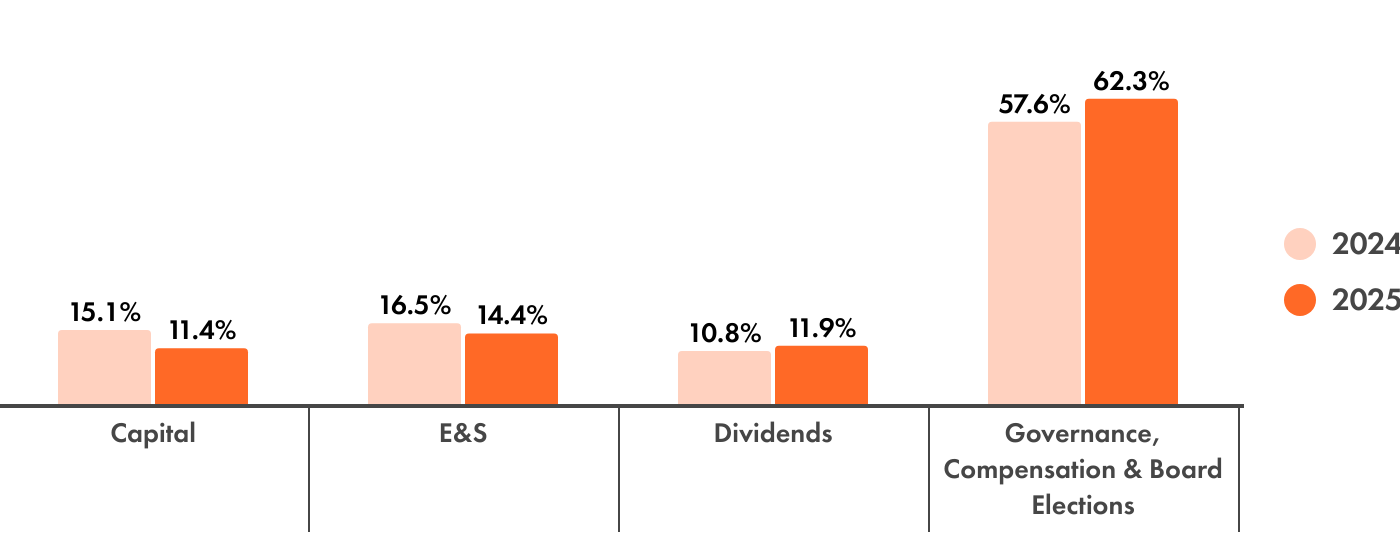

The increase in the overall number of shareholder proposals reflects a heightened focus on governance and dividend issues (Figure 2). Moreover, a series of high-profile shareholder campaigns seeking board changes underscores the growing influence of shareholder activism on corporate governance practices among Japanese companies.

Figure 2. Shareholder Proposals by Category, 2024-2025

Source: Glass Lewis Research. Note: Data as of Jan. 1 to June 30 for the 2024 and 2025 proxy seasons.

Activism Example One: Shareholders Seek Dividend Authority

The investor push for greater capital efficiency, and greater influence over capital strategy, led to Eiken Chemical, GungHo Online Entertainment, Japan Pure Chemical and Stella Chemifa, among other companies, facing proposals calling for increased shareholder input on dividend distribution at their 2025 AGMs.

These companies all have articles of incorporation which exclusively grant authority to declare dividends to the board, meaning that these companies effectively impeded shareholders’ ability to submit shareholder proposals regarding dividends.

The main rationale put forth by the proponents was that the current articles of incorporation did not reflect shareholders’ intentions regarding dividend distribution. In addition, the shareholder proponent at Eiken argued that allowing shareholder input on dividend distributions is general market practice. They cited a study which found that of 1,902 listed companies, only 12.3% granted the board exclusive authority over dividend distribution.3

In response, the arguments put forth by the companies noted that the board of directors had an information advantage and were best placed to decide on dividend amounts in a flexible manner.

Ultimately, the proposal to amend Eiken articles passed with over 70% support. Given that the shareholder proponent at Eiken only held approximately 10.5% of the company’s issued share capital, it is evident that most other minority shareholders were supportive of the proposed changes.

Similar proposals at GungHo (49.3% support), Japan Pure Chemical (48.7%) and Stella Chemifa (47.2%) all fell short of the required two-thirds majority. However, as the proponents’ holdings at these companies ranged between 4% and 16%, these results similarly indicate significant backing from minority shareholders.

Overall, this outcome reflects underlying investor support for greater influence over dividend decisions and sends a clear signal to boards on the need for proactive engagement with shareholders on this issue.

Activism Example Two: Contested Election at Fuji Media

Not all activism focused directly on improving capital efficiency. Concerns regarding governance practices and board accountability were also key drivers, including at Fuji Media Holdings (FMH), which held what was arguably the most closely scrutinized annual shareholder meeting of Japan’s 2025 proxy season.

The heightened interest followed a March 2025 third-party investigative report that exposed serious governance failures in FMH’s handling of sexual misconduct allegations involving a former employee and a celebrity regularly featured on Fuji Television programs.4 These failures had consequences beyond reputational harm. For the fiscal year ended March 2025, FMH posted a net loss of ¥20.1 billion ($127 million),5 partly due to the withdrawal of key sponsors and commercial partners — an outcome indirectly linked to governance issues at the subsidiary level.

In response, FMH unveiled a “Reform Action Plan” to enhance human rights protections, governance practices, and capital efficiency. Key measures included significant board refreshment and the elimination of long-standing internal advisory positions such as “sodanyaku” and “komon.” These roles are usually held by retired top executives such as former CEOs, who remain with the company in a less formal, often honorary, advisory capacity, providing guidance. The roles are often criticized in Japan for enabling former executives to retain influence without accountability.

While these reforms appeared promising, FMH’s long-standing structural weaknesses and inconsistent governance execution prompted Dalton Investments to submit a shareholder proposal nominating 12 alternative director candidates.

All company-nominated directors were elected with more than 80% support, while shareholder nominees received no more than 27%. Given the shareholder proponent only held approximately 7% of the company’s outstanding issued shares, this indicates a moderate amount of success in attracting support from other minority shareholders.

Management proposals, including the abolition of the sodanyaku position, were approved — leading some observers to view the outcome as a step toward governance modernization.

However, on June 27, just two days after the AGM, FMH disclosed in its Corporate Governance Report6 that Mr. Kanemitsu — Representative Director and President until the meeting’s conclusion — had been reappointed to a newly created “advisor” position with compensation. While the company had formally removed the sodanyaku title from its articles, the substance of the new role remains unclear. The timing and lack of explanation have raised questions about whether FMH’s reforms represent genuine change or a rebranding of entrenched practices.

By appointing a recently retired top executive to an advisory capacity immediately after abolishing similar legacy positions, FMH risks undermining the credibility of its governance commitments and sending mixed signals to shareholders.

Following the meeting, President Shimizu emphasized that the formation of a Nomination and Remuneration Committee had strengthened FMH’s governance framework, enabling implementation of the Reform Action Plan. However, retaining Mr. Kanemitsu in an advisory role leaves a critical question unresolved: can FMH credibly claim to have broken from past practices while preserving mechanisms that allow former leaders to exert influence behind the scenes?

FMH’s pledge to pursue governance-focused management will ultimately be assessed not by the formal adoption of new structures, but by the extent to which these changes deliver genuine accountability and transparency. Shareholders and the market will be watching closely.

Activism Example Three: Vote No Campaign at Taiyo

In the Japanese market, shareholders have historically been supportive of management. And it is relatively rare for proposals seeking the reappointment of management nominees to fail, absent serious misconduct. Therefore, the failure of Taiyo’s representative director, president, and CEO, Mr. Sato, to secure majority shareholder support for his reappointment marks a significant moment that may prompt companies to rethink how they engage with their shareholders going forward.

The surprising outcome was the result of a shareholder campaign led by Oasis Management Company (Oasis), Taiyo’s second-largest shareholder with an approximate 11.1% stake. Oasis also holds a significant stake of approximately 11.5% in DIC Corporation (DIC), Taiyo’s largest minority shareholder, which itself owns approximately 20.2% of the company’s issued share capital.

The main rationale put forth by Oasis concerned Taiyo’s strategic relationship with DIC, in addition to strategic decisions to invest in the medical and pharmaceuticals business.7 Furthermore, Oasis raised concerns regarding the company’s executive compensation practices, and what it views as governance failures under Mr. Sato’s leadership.

In response, the company argued that the strategic relationship has generated various synergies, while the strategic direction to invest in the medical and pharmaceuticals business was undertaken to diversify and stabilize earnings. Moreover, the company noted that Mr. Sato’s remuneration was not overly excessive and was designed to be closely tied to business performance, while further disputing the claims of governance failures put forth by Oasis.

Another significant source of concern was the company’s response following the issuance of an arrest warrant against then statutory auditor, Mr. Oki, by the Thai government in relation to the creation and submission of forged documents. The board defended its response by stating that, as the issuance of an arrest warrant does not constitute a final conviction, it prioritized a thorough investigation of the facts and the implementation of preventative measures, rather than taking immediate disciplinary action against Mr. Oki.8

Though an arrest warrant is not a final conviction, many investors likely considered it sufficient grounds for disciplinary action, especially in a role as critical as a statutory auditor. These concerns were compounded by the broader lack of transparency surrounding the matter, including the absence of meaningful and timely disclosure about the incident or the subsequent investigation.

While Oasis’s shareholder proposal narrowly failed to pass, shareholders appeared convinced by Oasis’s arguments, as Mr. Sato failed to secure majority support for reappointment to the board.

Conclusion

With investors becoming more open to employing activist tactics like submitting shareholder proposals and conducting ‘vote no’ campaigns, the pressure on Japanese boards is increasing. With the 2026 proxy season looming, engagement and disclosure that demonstrates companies are listening to shareholder concerns and addressing key indicators can help to meet evolving expectations on governance practices and capital efficiency. With activism intensifying, failure to meet those expectations could expose companies to a costly contested proxy campaign, or even the reputational damage that comes with losing a management vote.

Notes and References

1 Keohane, David. “Japan’s activists grapple with a new problem — success”. Financial Times. January 13, 2026. Accessed January 20, 2026. https://www.ft.com/content/a269c489-2e1c-4363-9fe8-03f42a77b53e

2 Glass Lewis. Japan Proxy Season Review 2025.

3 Eiken Chemical Co., Ltd. Notice of Convocation of the 87th General Meeting of Shareholders. June 9, 2025. Page 22. https://www.eiken.co.jp/uploads/en/news/common/20250602.pdf

4 Inoue, Yukana. “What the Fuji TV third-party probe uncovered.” Japan Times. April 1 2025. Accessed January 20, 2026. https://www.japantimes.co.jp/news/2025/04/01/japan/media/fuji-corporate-culture/

5 Fuji Media Holdings, Inc. Securities Report, Fiscal Year 2025. Conversion as of Jan. 20, 2026. https://disclosure2dl.edinet-fsa.go.jp/searchdocument/pdf/S100W5GP.pdf

6 Fuji Media Holdings, Inc. Corporate Governance Report 2025. https://www2.jpx.co.jp/disc/46760/140120250627502291.pdf

7 Oasis Management Company Ltd. “Better Corporate Governance for Taiyo HD.” Accessed January 20, 2026. https://static1.squarespace.com/static/6811814d5a49f0360b2a80ff/t/681ae549fb46871ebe4f3672/1746593117883/Taiyo_Corp_Gov-EvShare.pdf

8 Taiyo Holdings Co., Ltd. Notice of 79th Ordinary General Shareholders’ Meeting. May 30, 2025. Page 16. https://www.taiyo-hd.co.jp/en/investor/irnews/news20250529102993/main/0/link/en20250528_04.pdf