Key Takeaways

- While a widespread "DEXIT" has yet to materialize, state-to-state reincorporations by U.S. public companies remain in the spotlight.

- Of the 26 reincorporation proposals that went to a vote in the second half of 2025, 16 involved existing companies and 10 involved a SPAC or other business combination.

- Among existing companies, the most common reasons cited for reincorporating were the jurisdiction’s legal environment (81%), Delaware’s franchise taxes and fees (50%), litigation risk (38%) and business operations (25%).

- Only 29% of the reincorporations from the 2025 post-season involved significant or controlling shareholders, compared to 55% during the 2025 proxy season.

- Although average support for reincorporation proposals rose to 86% in the post-season compared to 82% in proxy season, more reincorporation proposals were not approved by shareholders (four, vs. two during proxy season).

State-to-state reincorporations have been in the spotlight recently, as U.S. companies and shareholders consider which jurisdiction provides the greatest benefits, while states compete to attract and retain them.

In response to speculation that companies would leave Delaware due to court decisions viewed as unfavorable to controlling shareholders and the risk of litigation, Delaware, Nevada, and Texas each adopted new legislation intended to attract incorporations or retain existing ones. Despite fears of a widespread “DEXIT,” observations from the 2025 proxy season indicated that reincorporations have generally been limited to companies with significant or controlling shareholders and other unique considerations.1

This article examines trends in reincorporations from the second half of 2025, including where companies are reincorporating, the rationales cited by their boards, and whether companies with significant or controlling shareholders continue to drive the increase in reincorporation activity.

Reincorporation Proposals and Common Rationales: 2025 Post-Proxy Season

During the 2025 post-season,2 we covered 26 more reincorporation proposals (vs. 29 in 2025 proxy season). Additionally, as noted below, cryptocurrency exchange Coinbase reincorporated from Delaware to Texas by written consent, without putting the move to a shareholder vote.3 A closer examination of the volume reveals that 10 of the reincorporation proposals were tied to a business combination or merger, compared to just four such proposals during proxy season. As such, this article will generally focus on the reincorporation proposals that were not tied to a business combination or merger.

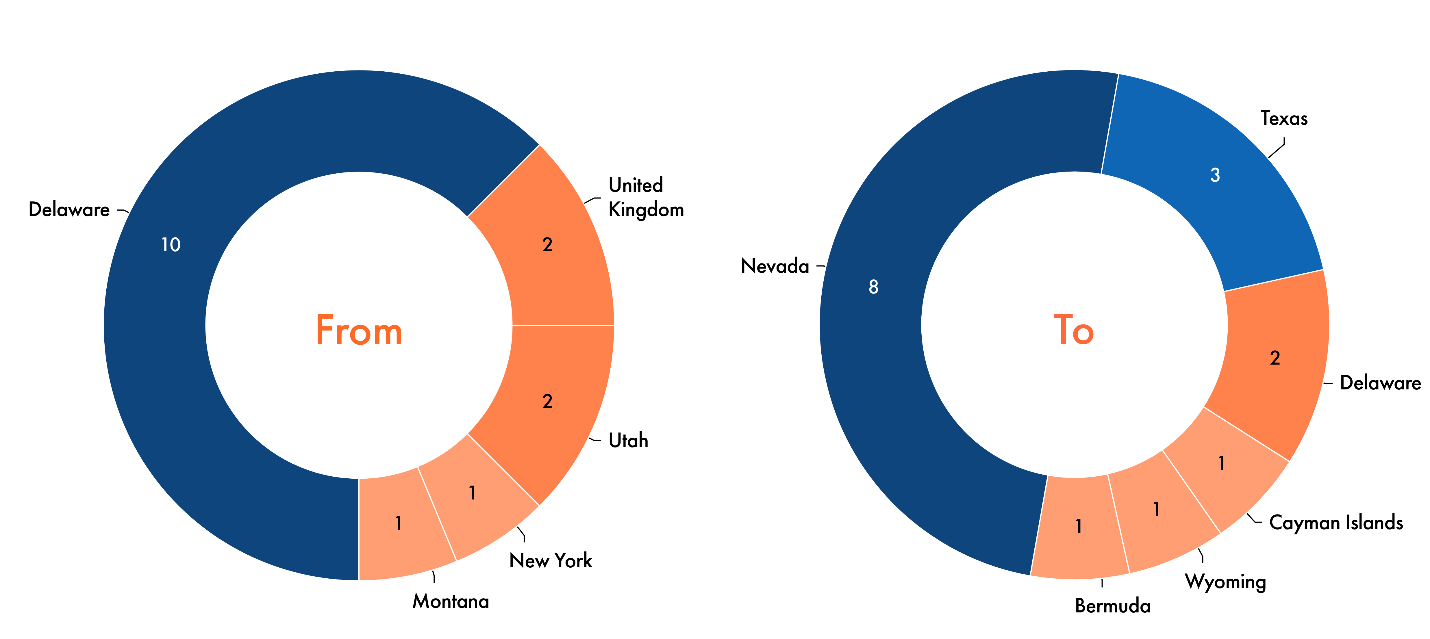

Ten of the 16 companies (Figure 1) with reincorporation proposals unrelated to a business combination on their ballots proposed leaving Delaware (63% vs. 64% during proxy season). Of the 10 companies that proposed leaving Delaware, six sought to move to Nevada, while two proposed reincorporating to Texas.

In addition, one company proposed reincorporating to Texas and two to Nevada from states other than Delaware, while two companies proposed reincorporating to Delaware. Notably, just 29% of the reincorporations from the 2025 post-season involved significant or controlling shareholders, compared to 55% during proxy season.

Figure 1. U.S. Reincorporation Proposals in 2025 Post-Season

Source: Glass Lewis Research. Note: Reflects non-business combination related proposals.

The rationales companies cited as justification for their moves generally remained consistent with what we observed during proxy season, with some fluctuation in the frequency that certain rationales were used. Of the proposals, 81% (vs. 59% in proxy season) cited a jurisdiction’s legal environment, 50% (vs. 45% in proxy season) cited Delaware’s franchise taxes and fees, and 19% (vs. 34% in proxy season) cited director and officer (D&O) liability as part of the reasons why the company proposed a reincorporation. Comparably, the number of proposals citing business operations and litigation risk were nearly identical to proxy season, with 25% of companies citing business operations (vs. 24% in proxy season) and 38% citing litigation risk (vs. 38% in proxy season).

Figure 2. Common Rationales Proxy Season vs. Post-Season

Source: Glass Lewis Research. Note: Reflects non-business combination related proposals.

Risk posed by the general legal environment in states continued as the most cited rationale and increased in frequency by a significant margin (22% increase vs. proxy season), while concerns with D&O liability dropped in frequency (15% decrease vs. proxy season). This may indicate that states’ corporate laws and the shareholder rights provided by these laws were a more significant factor than risk from specific litigation targeting directors and officers, particularly following the amendments made by Delaware, Nevada, and Texas.

DEXIT: A Slow Drip

During the post-season, 63% of companies with reincorporation proposals on their ballots proposed leaving Delaware, nearly identical to proxy season (64%). However, there was a significant drop off in reincorporation activity among companies with significant or controlling shareholders (29% in post-season vs. 55% in proxy season), which may indicate that other factors drove reincorporation activity in the second half of 2025.

While reincorporation activity remains elevated and certain companies continue to leave Delaware, companies are not heading for the exits in large numbers. Many companies still choose to incorporate in Delaware. Of the 10 business combination-related reincorporation proposals mentioned earlier, eight chose to reincorporate in Delaware. All but one of these proposals involved special purpose acquisition companies (SPACs) combining with a private target, seven of which reincorporated from the Cayman Islands.

A New Frontier for Incorporation: Dillard's, Coinbase Global, and Forward Industries

Among the 16 existing public companies that sought to reincorporate, it appears that a desire for more favorable legal environments to suit unique business operations and strategies played a significant role. Specifically, each of the companies that reincorporated to Texas adopted certain provisions of the recently amended Texas Business Organizations Code (TBOC).4,5 While these provisions are widely viewed by investors as unfavorable to shareholder rights, they are generally considered business-friendly.6, 7

Three reincorporations highlight the trend of companies citing the general legal environment and their unique business needs as part of their rationale to relocate to jurisdictions where corporate statutes are more business-friendly.

Dillard's

At their special meeting in August 2025, Dillard’s, a controlled company, proposed a reincorporation from Delaware to Texas. Ahead of the meeting, the board considered whether the company should remain in Delaware or reincorporate to Nevada or Texas. The board concluded that reincorporation to Texas was in the best interests of shareholders, in part because of the company’s business operations in Texas. The board also considered Texas’s statute-focused approach to corporate law, the apparent increase in contingency fee-driven stockholder litigation in Delaware, and the resulting increase in insurance premiums for D&O insurance, particularly for controlled companies like Dillard’s.

The board ultimately concluded that the reincorporation may reduce the potential for opportunistic and frivolous litigation by opting in to certain newly amended provisions of the TBOC. Specifically, Dillard's sought to adopt the TBOC provisions providing an ownership threshold for plaintiffs to initiate derivative claims as well as submit shareholder proposals.

Coinbase

Coinbase Global, the largest U.S. based cryptocurrency exchange, also reincorporated from Delaware to Texas. Instead of holding a shareholder meeting, Coinbase’s reincorporation was executed by the written consent of its controlling shareholder.

Coinbase’s chief legal officer, Paul Grewal, published an op-ed in the Wall Street Journal to explain why the company preferred Texas to Delaware.8 As part of their rationale, Coinbase determined that Texas’ legal environment would provide a more favorable regulatory and judicial-review system that would support the company’s growth and innovation to achieve its mission to increase economic freedom in the world.

The op-ed also pointed to Texas’ codification of the business-judgement rule, which provides that directors may exercise their business judgment when acting in good faith, on an informed basis, in the company’s best interests, and lawfully, as an attractive aspect of the state’s modernized legal system. Texas’ business-friendly environment and support for cryptocurrency was a significant factor in Coinbase’s choice of jurisdiction.

Forward Industries

After Forward Industries’ August 2025 proposal to reincorporate from New York to Nevada did not receive the affirmative vote of a majority of shares outstanding, the company took a different path. In September 2025, Forward Industries closed a $1.65 billion private placement led by Galaxy Digital,9 a cryptocurrency-focused company, and intends to use the proceeds to purchase SOL, the digital asset of the Solana blockchain, and establish the company’s cryptocurrency treasury strategy.

Considering their new strategy, the board reassessed which states would benefit the company. At Forward Industries’ upcoming annual meeting in March 2026, the company has proposed a reincorporation from New York to Texas. Similarly to Coinbase, Forward Industries determined that Texas’ legal environment provided the best legal framework to enable the company to achieve its mission to grow and strengthen the Solana ecosystem, and that Texas’ support for crypto was a key aspect of the board’s decision in choosing Texas over a different jurisdiction.

The board also noted Texas’ codification of the business judgment rule as an example of the clarity and predictability that Texas’s code-based system provides. Forward Industries also elected to be governed by the provision of the TBOC that provides for an increased ownership threshold to submit shareholder proposals.

Vote Results on Reincorporation

Average support for reincorporation proposals rose to 86% in the post-season compared to 82% in proxy season, but remains below the average support level in 2024 and 2023. There were fewer companies with significant or controlling shareholders that sought to reincorporate in the second half of 2025, and all of their reincorporations received majority support from unaffiliated shareholders. By contrast, during proxy season several companies with significant or controlling shareholders did not receive majority support from unaffiliated shareholders for their reincorporation proposals.

Whether this was unique to the handful of companies with significant or controlling shareholders that proposed reincorporations in the second half of the year or part of a broader trend remains to be seen. And while average unaffiliated shareholder support rose, it still trended below the overall average. Dillard’s reincorporation proposal, for example, was supported by approximately 76% of the unaffiliated votes cast.

Although average support rose, so too did the number of failed reincorporation proposals. In total, four companies (vs. two in proxy season) proposed reincorporations that were not approved by shareholders. Three of these required the affirmative vote of a majority shares outstanding to pass. Notably, all four of the proposals that were not approved sought reincorporation to Nevada (two from Delaware and two from other states).

The Reincorporation Decision

Reincorporations have become a significant area of interest for shareholders. How companies respond to developments in corporate laws will likely be scrutinized by shareholders, who in some cases stand to lose certain rights depending on the chosen jurisdiction.

While controlled companies continue to leave Delaware in favor of other jurisdictions, companies are also identifying other factors that motivate their reincorporation decisions. Texas, for instance, has emerged as a state which offers certain benefits for companies whose operations and business revolve around cryptocurrencies.

Some established companies may choose to reincorporate to a state where the legal environment and corporate laws benefit their individual businesses and strategies. In contrast, newly public companies may tend to select Delaware as their jurisdiction of choice. This difference may in part be due to the unique benefits offered by Nevada and Texas, while Delaware remains the standard state of incorporation for most companies.

Going forward, boards will continue to evaluate the protections that various jurisdictions provide, while weighing what is in the long-term best interests of the company and shareholders. How these trends play out and evolve during the upcoming proxy season will continue to be a topic of interest.

Notes and References

1 Nolledo, S., Wenger, S., Wendt, A. “The State of US Reincorporation in 2025: The Growing Threat and Reality of “DEXIT.” Glass Lewis. October 9, 2025. https://www.glasslewis.com/article/state-of-us-reincorporation-2025-growing-threat-reality-dexit

2 The data included in this article is from the 2025 post-season period of July 1, 2025 to December 31, 2025.

3 Shareholder action by written consent is a legal mechanism that provides shareholders the ability to approve certain corporate actions, in lieu of a shareholder meeting, with the written approval from shareholders representing the minimum number of votes to pass the action at a meeting. This practice must be permitted by both the relevant state law and the company’s bylaws.

4 Tex. S.B. 29, 89th Leg., (2025). https://capitol.texas.gov/tlodocs/89R/billtext/pdf/SB00029F.pdf

5 Tex. S.B. 1057, 89th Leg., (2025). https://capitol.texas.gov/tlodocs/89R/billtext/pdf/SB01057F.pdf

6 Andrew Lucano, Alan S. Gaynor, James Dorough-Lewis, Jr., “Texas Adopts Business-Friendly Amendments to Its Corporate Code-A Response to Delaware?,” Seyfarth Shaw LLP, June 2, 2025, https://www.seyfarth.com/news-insights/texas-adopts-business-friendly-amendments-to-its-corporate-codea-response-to-delaware.html

7 Gallogly, Niko. “New Texas Laws Open a Wild West for Corporate Governance,” The New York Times, August 16, 2025, https://www.nytimes.com/2025/08/16/business/dealbook/texas-incorporation-delaware.html

8 Grewal, Paul. “Why Coinbase Is Leaving Delaware for Texas,” The Wall Street Journal, November 12, 2025, https://www.wsj.com/opinion/why-coinbase-is-leaving-delaware-for-texas-3a6c34a3

9 Forward Industries, Inc. Press Release. September 11, 2025. https://www.businesswire.com/news/home/20250910472556/en/Forward-Industries-Closes-%241.65-Billion-Private-Placement-in-Cash-and-Stablecoin-Commitments-to-Advance-Solana-Treasury-Strategy