Key Takeaways

- Compared to other European markets, French companies hold more types of say-on-pay votes. These votes occur more frequently, and have a stronger impact on pay outcomes.

- The impact includes the potential suspension or forfeiture of an executive’s variable and exceptional compensation following a failed “amounts” vote, reinforcing the link between shareholder approval and realized pay.

- The French pay voting regime predates SRD II, and reflects the influence of a variety of stakeholders, including French regulators and legislators and the AFEP-MEDEF code.

- While failed proposals are rare, investors have shown they are willing to use these mechanisms, particularly where the scope is limited to executive pay.

In the landscape of European executive remuneration, France stands out with a set of voting practices and disclosure requirements that diverge notably from its continental counterparts. Not only do French companies hold more types of say-on-pay votes than in other markets, these votes occur more frequently, and have a more direct impact on the amounts that individual executives are ultimately paid.

Moreover, whereas remuneration voting and oversight in most European countries was implemented in direct response to the European Union’s Shareholder Rights Directive (SRD II), France’s regime predates SRD II and has been influenced by a variety of stakeholders, including regulators, legislators and the AFEP-MEDEF code.

This article is broken out into three sections. The first section sets out the details and background of France’s approach to executive remuneration governance. The second section explores how it compares to regional peers in Europe. The concluding section examines shareholder voting data to discuss how this approach works in practice.

Remuneration of Corporate Officers in France: The Legislative Framework

French listed companies are uniquely required to obtain annual, binding shareholder approval for three different types of pay-related proposals, covering different aspects of the remuneration of their executive and non-executive corporate officers:

- Amounts: A retrospective vote on the actual amounts paid to the CEO and other executives in the past year in respect of variable and exceptional compensation.

- Remuneration Policy: The forward-looking pay structure.

- Remuneration Report: A retrospective vote on how that policy was applied in the past year.

Each type of proposal is explained in greater detail below, followed by a comparison to other European countries, and an analysis of how shareholders vote on these different types of proposals.

Amounts: Retrospective and Binding

Unlike in most other markets, companies must seek retrospective approval for the remuneration paid or granted in the past financial year. Specifically, these votes seek approval for the variable and exceptional remuneration paid or granted during the past fiscal year to the executive officers and the chair of the board. As each officer’s remuneration is put to a vote in distinct proposals, shareholders vote separately on the pay of each executive.

Impact of Failure to Approve: Neither variable nor exceptional amounts can be distributed should the relevant proposal be rejected by shareholders.1 This extends to grants awarded under long-term incentive plans and severance payments. Fixed remuneration, which would have been approved in the remuneration policy, may still be paid.

Remuneration Policy: Prospective and Binding

Similar to other European markets, French companies are required to obtain prospective approval for the remuneration policy for the following financial year. The policy outlines the fixed, variable, and exceptional components of total remuneration and benefits of any kind. Boards can choose to submit a single, comprehensive policy vote, or separate policy votes for different executives.

Impact of Failure to Approve: Given its binding nature, in the event the policy does not receive the required majority support, companies will need to submit a revised version for approval or continue to implement the last version that was approved.2

Remuneration Report: Retrospective and Binding

Additionally, each year companies are required to seek retrospective approval for the implementation of their remuneration policy, as presented in the remuneration report. Like the votes on amounts described above, the remuneration report is also retrospective. However the votes are distinct. The former (i.e., the remuneration policy) requires a separate vote for each executive and only covers the variable and exceptional amounts paid or allocated to them during the previous fiscal year. The latter, the remuneration report, is approved as a whole, effectively covering both pay decisions made by the board and outcomes across all components of remuneration, for all corporate officers and non-executive directors, on an aggregate basis.

This report includes the total remuneration and benefits of any kind, divided into fixed, variable, and exceptional items paid or allocated to corporate officers in respect of their mandate during the past financial year. It may also include any commitments by the company resulting in remuneration, indemnities, or benefits resulting from termination or the changing of functions. The pay ratios between the CEO's remuneration and the median/average remuneration of its employees over the previous five years, along with a five-year comparison of pay and performance, must also appear in the remuneration report.

Impact of Failure to Approve: In the event the remuneration report is not approved by shareholders at the annual general meeting, the remuneration awarded to the members of the board of directors or the supervisory board will be suspended until a revised remuneration policy is approved. This only impacts the fees or other amounts paid in respect of board service, rather than any components of executive remuneration. In the event that the revised remuneration policy is also rejected, the suspended remuneration will be forfeited.3

Votes on Remuneration Across Europe

France’s approach to remuneration-related proposals varies significantly from other markets across Europe. It also predates them. Whereas most European markets only implemented regular remuneration votes in response to the SRD II directive, in France, annual individual amounts proposals were introduced in 2013, on an advisory basis, as part of an update to the AFEP-MEDEF governance code.4

The voting regime was subsequently strengthened and expanded by legislators in response to public outcry over the Renault board’s lack of responsiveness to a significant level of opposition to CEO Carlos Ghosn’s pay.5 On the same day, the European Commission, Council and Parliament reached an agreement regarding the SRD II directive, and the French law on transparency, anti-corruption and economic modernisation was announced.6

Sapin II made amounts proposals binding as of 2018. It also introduced annual, binding votes on the remuneration policy and its implementation (from 2017 and 2020, respectively). Cumulatively, these reforms make up a far more stringent application of the SRD II directive than in other European countries, while also retaining and enhancing France’s unique approach to approving executive pay outcomes on an individual basis.

France’s robust say-on-pay voting regime is perhaps unsurprising, given its approach to corporate governance more broadly. More recently, France became the first country in the European Union to fully transpose the Corporate Sustainability Reporting Directive (CSRD) into national law. While they ultimately backed away from doing so, French legislators also proposed to make Say on Climate votes compulsory for French-listed companies.

Types of Pay Votes

France is the only market in Continental Europe where listed companies must submit all three components of remuneration – the remuneration policy, the individual remuneration amounts, and the remuneration report – for shareholder approval. Other European markets typically require solely a vote on the policy and either the amounts or the remuneration report.

Amounts Votes: France vs. Switzerland

Switzerland is the only other European market where amounts proposals are common. As it is not a member of the European Union, Swiss companies are not required to follow the SRD II directive, which gives them more discretion in how these proposals are implemented.

Unlike in France, where all amounts proposals are retrospective, Swiss companies may choose whether they wish to implement the amounts proposal retrospectively or prospectively. Whereas French amounts proposals always cover variable and exceptional pay and are submitted separately for each executive, Swiss amounts proposals may be presented on an aggregate basis, covering all executives; and each component may be presented individually (for example, fixed salaries, the short-term incentive plan, and the long-term incentive plan may all be put up for a vote in distinct proposals). In practice, Swiss companies typically cover all executives and components in one aggregate amounts proposal.

Vote Cadence

While all remuneration-related votes take place on an annual basis in France, most other European markets hold remuneration policy votes every three or four years, in line with SRD II requirements.

Impact of Failure to Approve

The impact of shareholder opposition to remuneration-related proposals varies across European markets, depending upon whether they’re binding or advisory in nature:

- Advisory proposals provide feedback to the board, but do not carry any direct consequences.

- Binding proposals are required to be resubmitted at the next general meeting. For prospective proposals, such as policy proposals, the existing policy remains in place. For retrospective proposals, such as proposals regarding individual amounts, payments may be suspended or forfeited.

As all remuneration-related proposals are binding in France, they require the support of a majority of shareholders before non-fixed remuneration (including any severance) will be paid or a policy approved. However, in most other European markets, the remuneration policy alone is binding while the remuneration report proposal covering the policy’s application is advisory, with no impact on amounts paid.

The table below displays the occurrence of the various types of remuneration-related proposals across various markets in Continental Europe as well as the UK. Where proposals are mandatory, listed companies are required to include them as an agenda item at a pre-defined interval, whereas they can choose whether to do so for optional proposals.

Table 1. Remuneration Proposals Across European Markets

Source: Glass Lewis Research.

Shareholder Voting on Executive Remuneration

It is relatively rare for French shareholders to reject remuneration proposals. Among large- and mid-cap companies both listed and incorporated in France, no retrospective consultative proposals have been rejected since 2023, when two proposals failed to achieve majority support.

Nonetheless, shareholders in France actively engage with executive remuneration proposals, and will demonstrate their concerns by voting against any element of backward- or forward-looking remuneration they find problematic, knowing they have a direct impact on remuneration decisions.

Figure 1 shows the vote results for remuneration proposals submitted by French blue-chip and mid-cap companies in 2025. In particular, the graph shows how each type or proposal fared, grouped by the level of shareholder support received.

Figure 1. Shareholder Support for Remuneration Proposals in 2025

Source: Glass Lewis Research.

Notably, the more specific the scope of the proposal, the more likely shareholders were to dissent. Both average opposition rates and the likelihood of significant opposition were significantly higher on individual amounts and the remuneration policy than on remuneration reports.

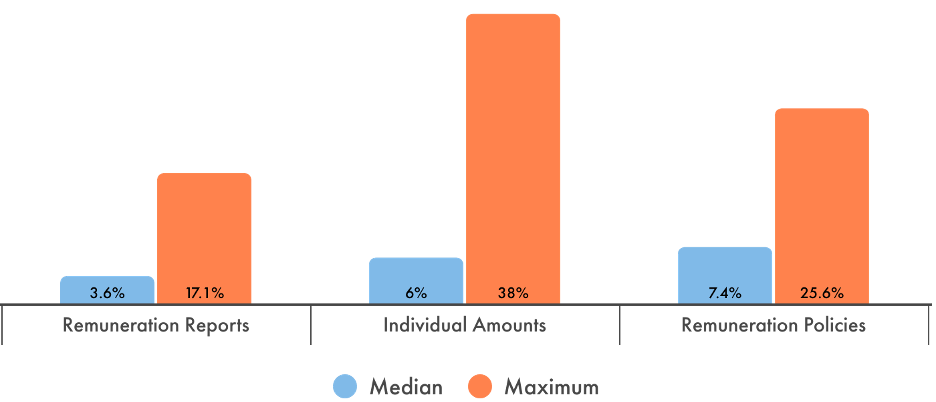

Since the current regime was implemented, no remuneration report proposals have been rejected. Moreover, in 2025, the median opposition for CAC 40 remuneration reports was only 3.6%, with a high of 17.1%. In comparison, the median dissent demonstrated towards individual amounts proposals at CAC 40 companies during the same period was 6%, reaching 38%, while the median for remuneration policy proposals amounted to 7.4%, with up to 26% for the most contested proposal (Figure 2).

Figure 2. Shareholder Opposition to CEO Remuneration Proposals at CAC 40 Companies in 2025

Source: Glass Lewis Research.

The tendency for shareholder opposition to be focused on individual amounts and remuneration policies may reflect that these proposals (and the consequences of their rejection) are directly linked with executive compensation. By contrast, if a remuneration report were rejected, the primary consequence would be for non-executive director fees to be suspended and potentially forfeited. The remuneration of board members is often viewed as unproblematic.

Conclusion

France’s legislative and regulatory framework for executive remuneration is more stringent than those in other Continental European markets. By requiring annual, binding shareholder votes on the remuneration policy, its implementation, and the individual amounts paid to executives, the framework gives investors an unusually direct role in shaping pay outcomes and enforcing accountability. While failed proposals are rare, investors have shown they are willing to use these mechanisms, particularly on proposals where the scope is limited to executive pay. The potential suspension or forfeiture of variable and exceptional compensation following a failed vote further differentiates France from its European peers and reinforces the link between shareholder approval and realized pay.

Looking ahead, this model is likely to continue influencing how French boards structure executive remuneration and how investors approach proxy voting. Companies may remain cautious in calibrating incentives and pay outcomes, knowing that realized remuneration is subject to binding, retrospective scrutiny. For investors, the regime provides a powerful tool to assess pay-for-performance alignment and broader governance practices, suggesting that say-on-pay votes in France will remain a focal point for engagement and accountability going forward.

Notes and References

1 Article L.22-10-34 of the French Commercial Code.

2 Article L.22-10-76 of the French Commercial Code and Article L.22-10-8 of the French Commercial Code.

3 Article L.22-10-9 of the French Commercial Code and Article L.22-10-34 of the French Commercial Code.

4 Reuters. “French business lobby adopts new guidance on 'say on pay'”. June 16, 2013. https://www.reuters.com/article/idUSBRE95F0FG/

5 Dessaint, Loic. “The French parliament adopts the binding the annual Say on Pays vote.” Proxinvest. June 20, 2016. https://www.proxinvest.com/en/2016/06/20/3791/

6 Autorité des marchés financiers. “French and European ‘Say on Pay’ Regimes.” May 3, 2017. https://www.amf-france.org/en/news-publications/news/french-and-european-say-pay-regimes