Tracking Shareholder Proposals and Company Exclusions: Mid-Season Observations

Subscribe

Key Takeaways

- In the absence of SEC no-action relief, companies are moving to exclude far fewer shareholder proposals — which has largely offset the reported decline in the number of proposals being filed.

- The proponent's identity matters: companies are seeking to omit more proposals submitted by individual shareholders, while allowing proposals from institutional and “anti-ESG” proponents onto the ballot.

- The SEC's current "no objection" approach creates a more complex landscape for engagement and negotiation, while leaving boards (and the SEC itself) exposed to litigation.

- The number of shareholder proposals covering social topics continues to decline, while the proportion focusing on governance continues to surge.

How has the SEC’s new approach to no-action requests1 impacted the shareholder proposal landscape? It’s a question that Glass Lewis is monitoring throughout this year’s U.S. proxy season.

Four months into the year, and with proxy season at its peak, some notable trends are emerging. In the second instalment of an ongoing series on shareholder proposals and company exclusions, we share what we’ve observed at meetings held through April 30.

Proposal and Exclusion Request Volumes

Key Takeaway #1: In the absence of SEC no-action relief, companies are moving to exclude far fewer shareholder proposals — which has largely offset the reported decline in the number of proposals being filed.

A lot of attention has been paid to how the SEC’s November 2025 decision to stay out of no-action relief is reshaping proxy season. While it’s true that proponents have filed fewer shareholder proposals in 2026 than in recent years, it’s not clear that this has anything to do with the SEC’s new guidance. Additionally, the impact of that decline on the number of shareholder proposals that have actually gone to a vote has largely been offset by a change in how companies are approaching proposal exclusions. Although the number of proposals filed is down by as much as 47%,2 the number of shareholder proposals that went to a vote is only down by approximately 8% through April 30, compared to 2025. That’s because over the same period, the number of exclusion requests filed by companies dropped by nearly half (Figure 1).

Figure 1. Number of Shareholder Proposals and Exclusion Notices for AGMs Through April 30

.png)

Source: Glass Lewis Research with no-action requests compiled from SEC.3 Note: Covers shareholder meetings held through April 30. Excludes withdrawn exclusion notices, and 2026 data excludes notices filed prior to November 17, 2025.

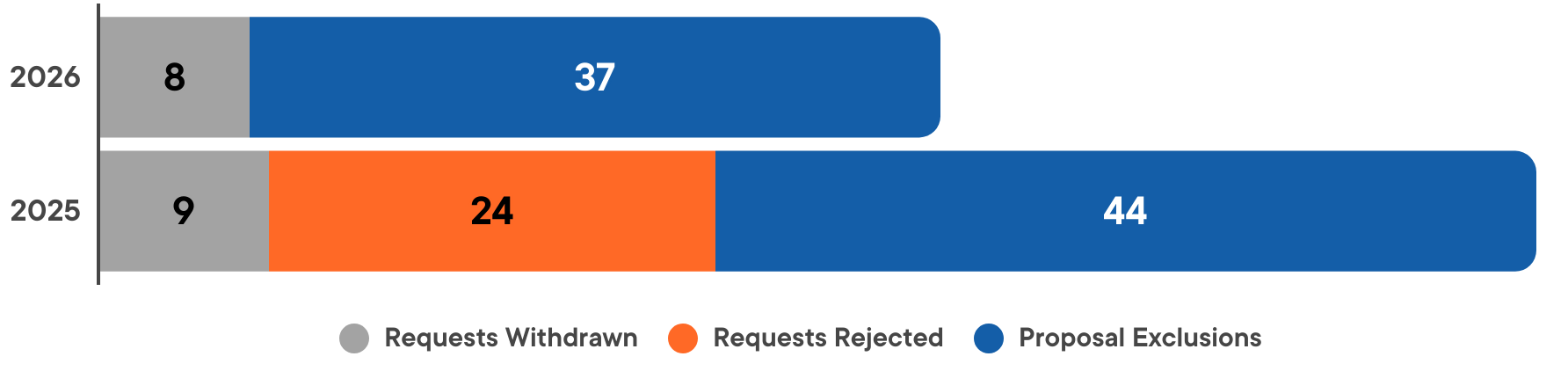

Figure 2 below provides a breakdown of total exclusion requests, indicating how many were rejected by the SEC or withdrawn. It’s notable that the number of proposal exclusions is down so far this year even though no 2026 requests have been rejected.

Figure 2. Breakdown of Rejected and Withdrawn Exclusions Notices at AGMs Through April 30

Source: Glass Lewis Research with no-action requests compiled from SEC.4 Note: Data for 2026 excludes notices filed prior to November 17, 2025.

A look at the timing of these proposals and exclusions may shed further light on shifting practices. The volume of proposal exclusions in January and February was stable from year to year, before dropping by 55% for the months of March and April. This may indicate greater willingness to allow proposals to go to a vote, even though the bar for exclusions is now theoretically lower.

By contrast, while the total number of shareholder proposals is down year-on-year, the number that went to a vote in March and April 2026 (97 proposals) was actually slightly higher compared to 2025 (95 proposals). That means the year-on-year decline in shareholder proposal volumes occurred at the start of 2026. At that point, it was likely too early for the change in SEC guidance to have had an impact, given that it was only announced in mid-November.

Instead, the overall decline in shareholder proposal volumes from last proxy season likely reflects the same ongoing trends that have driven similar declines over the past several years. These trends include a prior change in SEC guidance that allowed for the exclusion of more environmental and social proposals, growing pushback on ESG, and the widespread success of prior shareholder proposals in establishing market norms and addressing investor concerns on many of the topics that have been the subject of recent activism.

How Companies Are Leveraging Proposal Exclusion

Key Takeaway #2: The proponent's identity matters: companies are seeking to omit more proposals submitted by individual shareholders, while allowing proposals from institutional and “anti-ESG” proponents onto the ballot.

A look at the breakdown of proponents suggests that companies may be taking a different approach to proposal exclusions in 2026, depending on who filed the proposal. While the mix of proponents among proposals that went to a vote remained largely stable from 2025 to 2026, the pool of proponents whose proposals were targeted for exclusion has changed significantly this season (Figure 3).

Figure 3. Breakdown of Proponents on Exclusion Requests and Shareholder Proposals Going to Vote, 2025 vs. 2026 For Meetings Through April 30

Source: Glass Lewis Research with no-action requests compiled from SEC. Note: Excludes proposals where the proponent is not disclosed.

Notably, for AGMs through the end of April, no proposal submitted by an institutional investor has been omitted this proxy season (compared to five last proxy season). Moreover, over this period the proportion of exclusion notices covering proposals submitted by advocacy or religious organizations, as well as by mission-driven investors, is down 50% from 2025. This primarily relates to proposals from so-called “anti-ESG” proponents. Through April of last year, companies sought to exclude 22 proposals filed by these organizations, making up more than one-third of the total exclusion notices filed in respect of meetings held in that period. This year, companies have only sought to exclude six proposals submitted by these proponents, and all six of these requests have subsequently been withdrawn.

Instead, companies have targeted individual proponents – and one individual in particular, John Chevedden. The proportion of exclusion notices that relate to proposals submitted by this prolific proponent grew to more than half of the total so far in 2026, with the proportion that relate to all individual proponents up to over 70%.

Proposal Topics for Exclusion

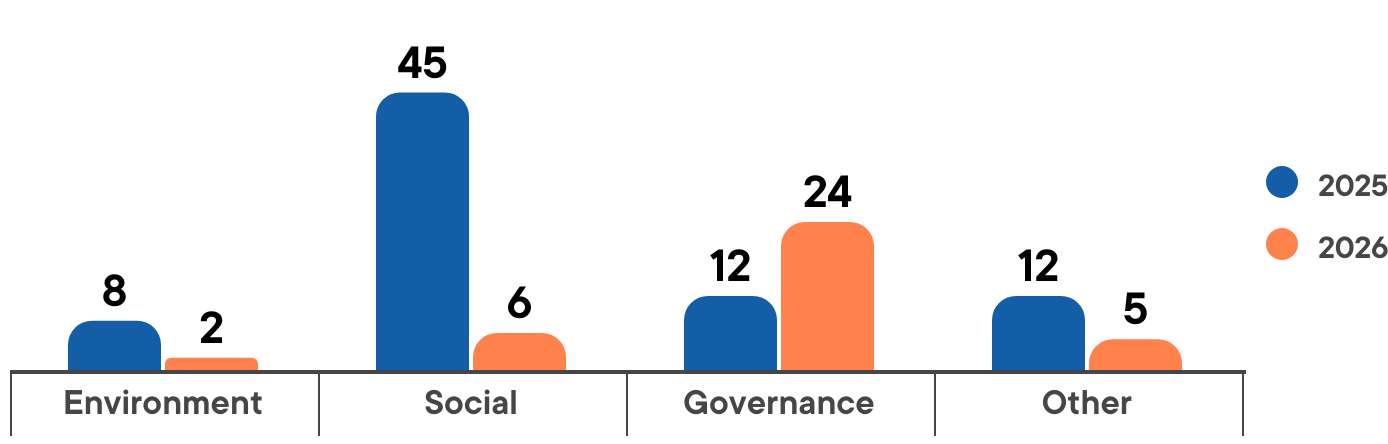

The types of shareholder proposals being targeted for exclusion is also shifting. In particular, companies are focusing much more on governance proposals, with the number of exclusions doubling from 2025 to 2026, and less on environmental and social proposals, for which the number of exclusion notices went down by 85% (Figure 4).

Figure 4. Exclusion Notices by Proposal Topic, 2025 and 2026 Through April 30

Source: Glass Lewis Research with no-action requests compiled from SEC.

Looking at a breakdown of governance-related shareholder proposals that have either been targeted for exclusion or gone to a vote (Figure 5), this year companies appear to be focusing on excluding proposals seeking to establish an independent board chair and/or separate the chair and CEO positions, or establish simple majority voting, while letting proposals regarding shareholders’ right to call a special meeting or act by written consent go to vote.

Figure 5. Breakdown of Governance Proposals Through April 30 by Topic

Notably, several companies that received the same proposal calling for them to establish “an enduring policy” of separate chair and CEO positions (in each case submitted by John Chevedden) have each cited use of the word “enduring” as a basis to exclude the proposal. Whereas in prior years SEC staff could have stepped in to request that the language of the proposals be amended, with the agency declining to review no-action requests, these proposals have simply been excluded.5

To some extent, the mix of topics targeted by exclusion notices reflects the overall mix of proposals. In particular, the number of governance proposals being submitted is up compared to last year, and the number of E&S proposals being submitted is down (see Figure 7, below). However, while these changes in proposal volume likely influenced the 2026 mix of exclusion notices, they do not fully explain it. Beyond proposal volume, the low level of shareholder support that many E&S topics received last proxy season may have left companies more willing to let these proposals go to a vote. In addition, the apparent reluctance to target anti-ESG proponents this year may be a factor, as these firms have submitted more than half of 2026 E&S proposals (see Figure 8 below).

Basis for Exclusion

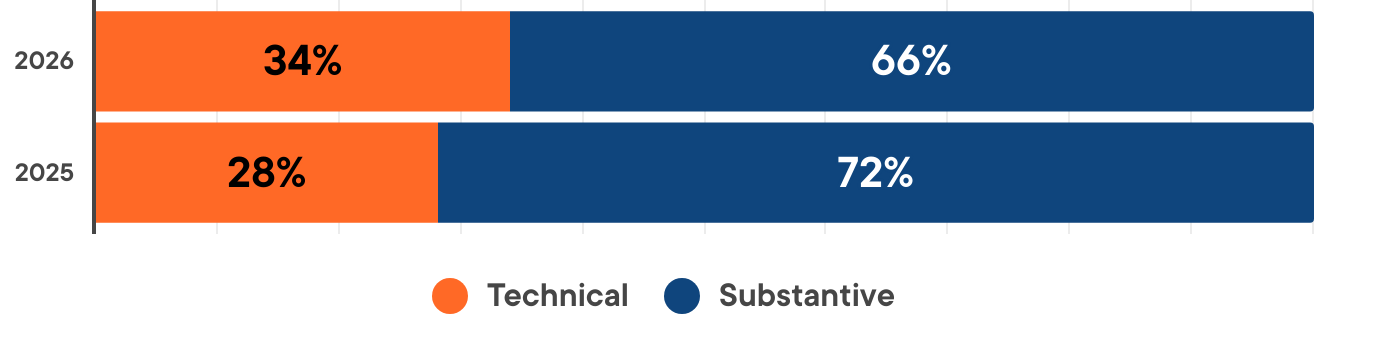

As discussed in our pre-season observations,6 the SEC’s new approach could also have an impact on the grounds companies cite to exclude proposals. While the margin is not definitive, through the end of April, more companies are relying on procedural or technical reasons to exclude proposals compared to 2025 (Figure 6).

Figure 6. Basis Cited by Companies for Exclusion of Shareholder Proposals

Source: Glass Lewis Research with no-action requests compiled from SEC.

The decision to focus solely on more clear-cut procedural issues could indicate that, absent cover from SEC staff, companies may be looking to avoid relying on substantive reasons, which can be open to debate.

Investor Responses to Proposal Exclusions: Litigation and Negotiation

Key Takeaway #3: The SEC's current "no objection" approach creates a more complex landscape for engagement and negotiation, while leaving boards (and the SEC itself) exposed to litigation.

BJ’s Wholesale Club has been subject to both litigation and some novel negotiation tactics after it sought to exclude two environmental proposals from New York State Common Retirement Fund (covering deforestation risk)7 and Trillium Asset Management (covering greenhouse gas, or GHG, emissions).8

In the latter case, Trillium responded to the exclusion notice by announcing its intent to utilize the company’s advance notice bylaws to submit the GHG proposal, as well as other “good governance” proposals, outside of Rule 14a-8. Rather than face a wide-ranging contest, the company agreed to include Trillium’s original GHG emissions proposal in its AGM proxy.

In the former case, the proponent took a more traditional approach, filing a lawsuit and ultimately receiving a preliminary injunction from a federal court in Massachusetts that requires the company to include its deforestation risk proposal on the AGM agenda.

Other lawsuits at AT&T, Axon Enterprises and PepsiCo have been similarly effective in pushing back on those companies’ attempts to exclude shareholder proposals:

- AT&T reached a settlement with the proponent, a group of New York City pension funds,9 allowing a resolution on workforce diversity disclosure to go to a vote after excluding it on the basis that it covered ordinary business.

- Similarly, PepsiCo reached a settlement with PETA after initially excluding a proposal requesting reporting on the treatment of animals in company and partner supply chains on procedural grounds.10

- The Nathan Cummings Foundation settled its suit against Axon Corporation after a judge ordered the two parties to compromise over a request for political contributions reporting. Under the settlement, Axon “agreed to broad and detailed annual disclosure and transparency on its direct political spending.” 11

However, not all legal challenges by proponents have been successful:

- UnitedHealth excluded a proposal calling for reporting on the healthcare impact of the company’s recent acquisitions. The proponent sued, but a judge agreed that the request was too broad and served to micromanage the company. Following the judgment, the proposal has been excluded from the company’s upcoming AGM.12

- Chubb Limited was sued by As You Sow after it moved to exclude a proposal requesting that the company explore pursuing subrogation claims for climate-related lawsuits. In late March a judge found that As You Sow had not yet demonstrated that it was entitled to emergency injunctive relief, giving the proponent 120 days to properly serve the company; however, Chubb has now filed its notice of meeting, and the proposal appears to have been excluded.13

ICCR vs. SEC

Companies are not the only parties that have been subject to litigation. In March 2026, the Interfaith Center for Corporate Responsibility (ICCR) and As You Sow filed a complaint against the SEC itself, arguing that although the revised approach to no-action relief was issued as guidance, it functions as a legislative rule and weakens shareholder rights.14

The complaint includes three allegations:

- The approach illegally removes the company’s burden of persuasion and limits shareholders’ ability to respond to exclusion notices;

- The SEC did not provide sufficient justification for making the change; and

- The approach was approved without the required notice-and-comment period (which would apply to a legislative rule, as the plaintiffs view the guidance).

Litigation remains ongoing.

Proposals Still Making It Onto the Ballot

Key Takeaway #4: The number of shareholder proposals covering social topics continues to decline, while the proportion focusing on governance continues to surge.

In 2024, 33% of ESG shareholder proposals covered governance topics. That figure increased to 41% in 2025, and appears set to increase further this year. Through April 2026, more than half (54%) of the proposals going to a vote have been governance-related (Figure 7).

Figure 7. Breakdown of Shareholder Proposals by Topic

.png)

Source: Glass Lewis Research.

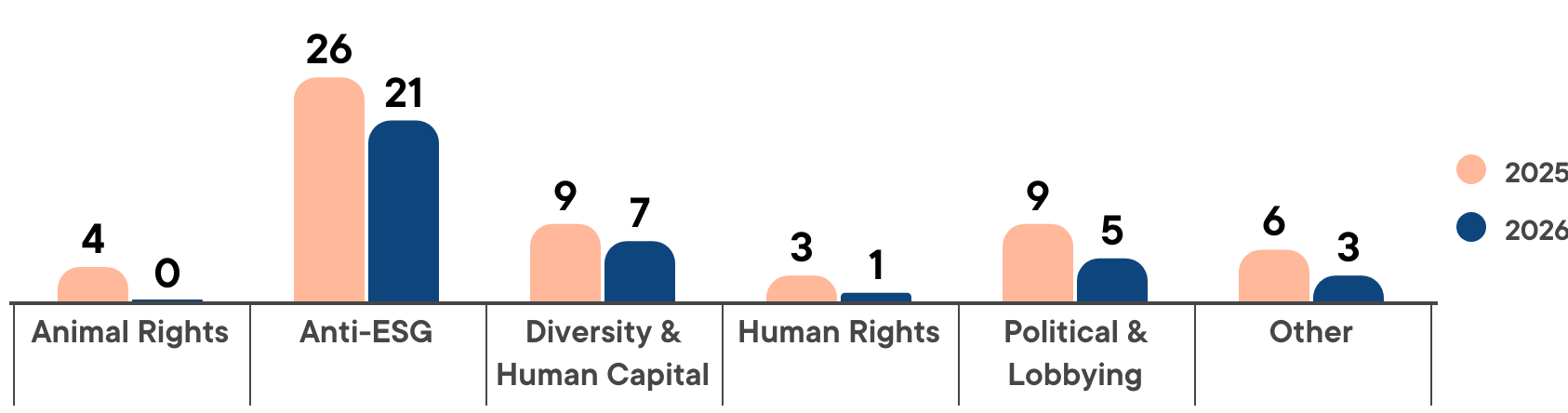

The complementary decline in the proportion of proposals covering E&S topics was exacerbated by a significant absolute drop in the number of social proposals, with only 37 so far in 2026 compared to 57 over the same period in 2025. Looking at sub-topics (Figure 8), this decline has been fairly consistent across the board.

Figure 8. Breakdown of Social Shareholder Proposals by Sub-Topic

Source: Glass Lewis Research.

In addition to being submitted less frequently, E&S proposals are increasingly likely to be submitted by anti-ESG proponents. So far in 2026, more than half of E&S shareholder proposals (27 of 52) have been submitted by anti-ESG proponents (Figure 9).

Figure 9. Proportion of E&S Proposals Submitted by Anti-ESG Proponents, to April 30

Source: Glass Lewis Research.

What Does This Mean?

Midway through proxy season, the new exclusion regime appears to be having a strong impact on company behavior. The number of exclusion notices is down significantly compared to 2025, and they have been targeted primarily at individual investors. Notably, companies appear to be cautious in their treatment of proposals submitted by certain proponents, particularly those who are well-funded or have shown willingness to stand their ground and negotiate. In addition, companies have focused more closely on governance proposals, and less on E&S proposals.

- For investors, these trends reinforce the importance of closely monitoring proposal topics, proponent profiles, and company responses.

- For proponents, while fewer exclusion requests may allow more proposals to reach a vote, the growing reliance on procedural challenges and the rise in litigation indicate that engagement strategies may need to adapt.

- For public companies, similarly, a reduced reliance on exclusion may support more direct shareholder engagement, but it also increases exposure to legal challenges and scrutiny around decision-making.

With thousands of meetings still to come, and more exclusion notices being filed every week, Glass Lewis will continue to monitor this topic and share our findings.

Notes and References

1 U.S. Securities and Exchange Commission. Division of Corporate Finance. "Statement Regarding the Division of Corporation Finance's Role in the Exchange Act Rule 14a-8 Process for the Current Proxy Season." November 17, 2025. https://www.sec.gov/newsroom/speeches-statements/statement-regarding-division-corporation-finances-role-exchange-act-rule-14a-8-process-current-proxy-season

2 As You Sow and Proxy Impact. "2026 Proxy Preview." Page 5. https://static1.squarespace.com/static/59f0ef404c326d3b5a4cf6a0/t/69dcfb0bca3729305ad1ef42/1776089867996/ProxyPreview2026_FIN_20260410.pdf

3 U.S. Securities and Exchange Commission. “2025-2026 Correspondence Under Exchange Act Rule 14a-8.” Accessed March 5, 2026. https://www.sec.gov/rules-regulations/shareholder-proposals/2025-2026-responses-issued-under-exchange-act-rule-14a-8

4 Ibid.

5 Interfaith Center on Corporate Responsibility. "Spotlighting Governance Failures by Companies During an SEC Oversight Vacuum. April 1, 2026." https://www.iccr.org/spotlighting-corporate-governance-failures/

6 Glass Lewis Editorial Team. “Tracking Shareholder Proposals and Company Exclusions: Pre-Season Observations.” Glass Lewis. March 6, 2026. https://www.glasslewis.com/article/tracking-shareholder-proposals-and-company-exclusions-pre-season-observations

7 Office of the New York State Comptroller. "DiNapoli Announces Victory in Shareholder Rights Lawsuit Against BJ's Wholesale." April 23, 2026. https://www.osc.ny.gov/press/releases/2026/04/dinapoli-announces-victory-shareholder-rights-lawsuit-against-bjs-wholesale

8 Trillium Asset Management. "With Protections for Shareholders Under Pressure, Trillium Takes Innovative Action to Defend Shareholder Rights." March 20, 2026. https://www.trilliuminvest.com/newsroom/with-protections-for-shareholders-under-pressure-trillium-takes-innovative-action-to-defend-shareholder-rights

9 NYC Comptroller. “NYC Pension Funds and AT&T Reach Settlement for Unlawful Exclusion of Shareholder Proposal Requesting Workforce Demographic Data Disclosure.” February 26, 2026. https://comptroller.nyc.gov/newsroom/nyc-pension-funds-and-att-reach-settlement-for-unlawful-exclusion-of-shareholder-proposal-requesting-workforce-demographic-data-disclosure/

10 PeTA. “Victory! PepsiCo to Allow Shareholder Vote on Bull-Abuse Concerns After Lawsuit.” February 24, 2026. https://www.peta.org/media/news-releases/victory-pepsico-to-allow-shareholder-vote-on-bull-abuse-concerns-after-lawsuit/

11 Gambetta, Gina. “Judge orders Axon to work with investor on “compromise” shareholder proposal.” Responsible Investor. March 3, 2026. https://www.responsible-investor.com/judge-orders-axon-to-work-with-investor-on-compromise-shareholder-proposal/

12 Banas, Nicole. "Judge denies injunction in suit over UnitedHealth shareholder proposal." WESTLAW Securities Enforcement & Litigation Daily Briefing. April 17, 2026. https://today.westlaw.com/Document/Ib21f57e53a9611f19818a90f0d2b683b/View/FullText.html

13 Memorandum Opinion. AS YOU SOW v. CHUBB LIMITED, No. 1:2026cv00734 - Document 23. March 31, 2026. https://law.justia.com/cases/federal/district-courts/district-of-columbia/dcdce/1:2026cv00734/289962/23/

14 Interfaith Center on Corporate Responsibility. "Investor Representatives File Lawsuit Challenging Unlawful Restriction of Shareholder Rights." March 19, 2026. https://www.iccr.org/investor-representatives-file-lawsuit-challenging-unlawful-restriction-of-shareholder-rights/