.png)

Key Takeaways

- Most public company boards in Finland, Iceland, Norway and Sweden use external shareholder nominating committees, typically composed of major shareholder representatives, rather than board committees composed solely of directors.

- On external committees, members are typically appointed by the company's largest shareholders, the incumbent committee, or the board as a whole.

- External committees provide direct access for major shareholders, ensuring that the committee’s nominations are generally backed by a large percentage of voting power.

- Not all large shareholders welcome this degree of influence. In particular, it's not uncommon for foreign investors to reject their seat on the committee to avoid potential trading restrictions.

- For minority shareholders, external shareholder committees typically provide less representation compared to board committees.

The nominating committee, as an agent for shareholders, is primarily responsible for the selection of objective and knowledgeable directors. In most markets, the nominating committee is typically composed of non-executive directors and constitutes one among other board committees. However, most public companies in Finland, Iceland, Norway and Sweden rely instead on external shareholder nominating committees,1 typically composed of major shareholder representatives.

This article provides an overview of how external nominating committees function and how they differ from board committees, examining the impact on the degree of accountability and representation afforded to different types of investors.

Committee Formation

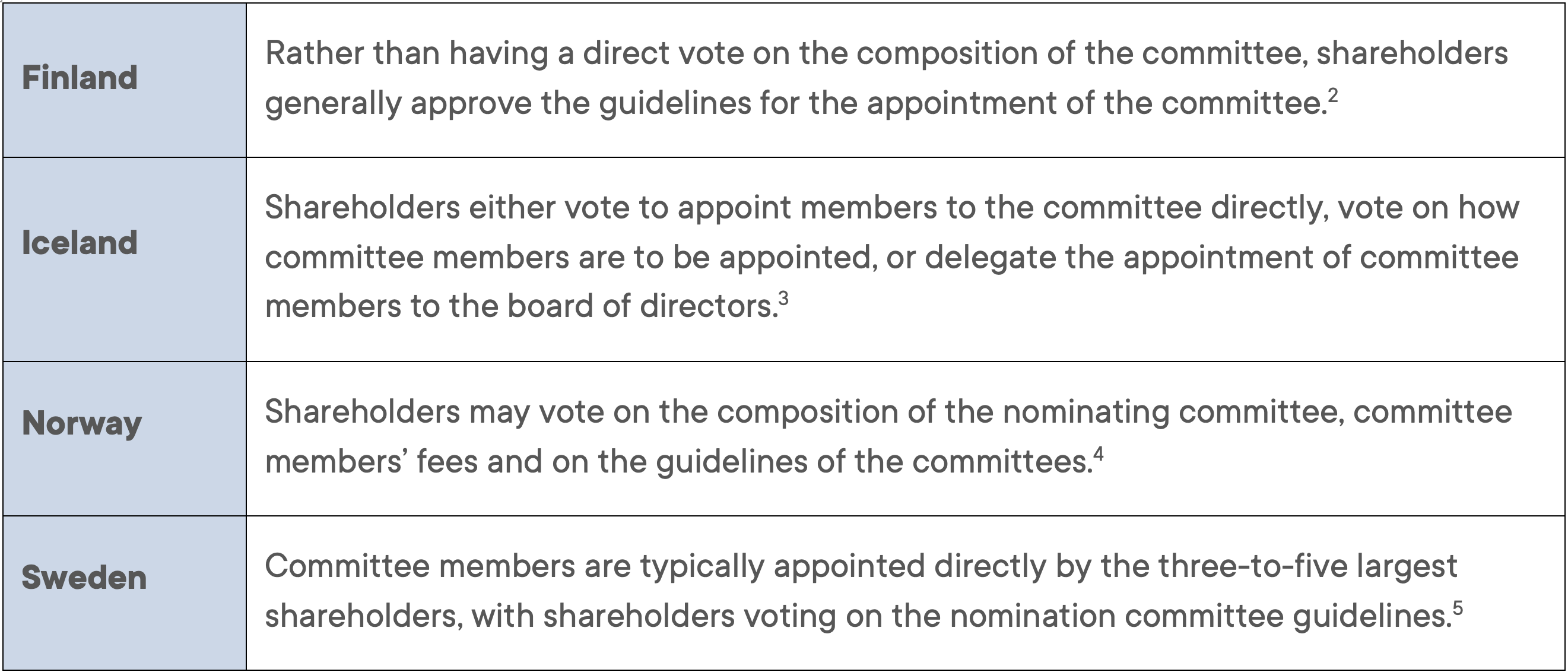

Whereas board committees are formed by, and composed of, directors elected to the board by shareholders, external committees can be formed in several ways (Table 1). In some cases, external nominating committee members are elected by shareholders, individually or as a slate; shareholders may also vote on the committee chair. In practice, this structure is very similar to board committees, except that the committee nominees may not be board members.

However, not all companies with external nominating committees allow shareholders to vote on the composition of the committee. Instead, committee members may be appointed by major shareholders, the incumbent committee, or the board as a whole. In these cases, shareholders do not directly elect the members, but are still able to weigh in on the committee through votes on its guidelines or the fees payable to members.

Table 1. Summary of External Nominating Committee Formation by Country

Source: Various. Compiled by Glass Lewis.

Committee Composition

The composition of external shareholder committees is fairly consistent. No executives should serve on the committee, and the majority of committee members should be composed of non-directors who are independent of the company.

However, there are differences from market to market. For example, in Sweden, the board chair typically serves on the external committee as a liaison; whereas in Norway, no board members are allowed to serve on the external nominating committee. Additionally, in Sweden there is a requirement that at least one member be independent of the company’s largest shareholder.

Committee Accountability

The different nominating committee structures and practices in these Nordic markets can pose challenges for shareholders who wish to effectively use their voting rights to voice concerns and hold these committees accountable. For board committees or external committees elected by shareholders, the process is usually straightforward, with annual elections allowing shareholders to express dissatisfaction with nominating committee members or the work of the committee.

When external committee members are appointed by major shareholders, the incumbent committee, or the board as a whole, the process can be more complicated. In these circumstances, shareholders typically get an opportunity to weigh in on the committee’s work and composition via a separate proposal to approve the nominating committee guidelines, a report from the committee, and/or its fee structure. While any shareholder can contact the committee to suggest a candidate for election to the board, this is, “a rare occurrence,” according to Oscar Börjesson, an ESG Analyst at Skandia Norden who has served on several Swedish nominating committees. Without a direct vote on committee members, rejecting the proposal covering the committee’s guidelines, report or fees may be the most effective way to express discontent on issues like board composition or diversity.

Investor Influence

How nomination committees are formed and how they are held accountable determines the level of shareholder involvement in the nomination process, which varies for different types of shareholders.

In the case of board committees, shareholders can only influence nominations by electing directors who will then participate in the committee’s decisions. While all shareholders have some level of influence via director elections, without a shareholder representative on the board, direct involvement in the committee’s work is limited. Because board committees are elected to represent all shareholders, regardless of size, they tend to offer more balanced representation.

Major Shareholders: Greater Direct Access

In contrast, external committees provide greater direct access for major shareholders, sometimes through direct representation on the committee. Even where major shareholders are not automatically granted a seat at the table, they still exert significant influence through a direct vote on either committee appointments or guidelines. This means that proposals submitted by the committee are generally backed by a large percentage of voting power, which Börjesson describes as the “biggest benefit” of the external shareholder committee model. “One of the nomination committee’s main roles is to submit proposals that will be approved, and this format facilitates that.”

While large shareholders often have direct representation, it isn’t directly proportional. Depending on the breakdown of the company’s share register, the largest holdings could span very different levels of ownership, but as Börjesson points out, “within the committee, each member has one vote, meaning the respective ownership levels don’t play a role.”

The influence of a single large shareholder may be further blunted by an expectation that the committee achieve a consensus. Börjesson notes that “In the rare cases where consensus is not reached, the nomination committee proposal generally states that the proposals were not unanimously approved."

Minority Shareholders: Less Representation

For minority shareholders, external shareholder committees typically provide less representation compared to board committees. Additionally, because shareholder committees often nominate their successors, there is a risk of limited refreshment, potentially entrenching certain interests over time. Börjesson outlines the concerns, and potential steps to mitigate them:

[I]t can be argued that this format is overly skewed towards larger shareholders and does not consider the perspective of all shareholders. The representation of smaller shareholders could be improved by the inclusion of more independent members, although for a proposal to pass, the largest shareholders will most likely have to be in favour. This is particularly relevant in the Nordics where it is common for companies to have a few large shareholders and many minor shareholders. ... [However,] smaller shareholder can always communicate with the committee and bring up suggestions.

Active Influence Creates Complications for Some Major Shareholders

Not all large shareholders welcome this degree of influence. In particular, Börjesson notes that, “[i]t's very common for foreign investors to reject their seat on the nomination committee.” This reluctance may reflect concerns that access to insider information could potentially create trading restrictions, or more broadly that taking such an active role is incompatible with the investor’s approach to stewardship.

We had a situation where we were maybe 20th largest owner in a company but were asked to be on the nomination committee as there were many foreign owners that held the larger percentage of shares. So the rest had said “thanks, but no thanks” and then we took that role.

With time and as the foreign ownership in the Swedish market has increased it is evolving into more and more of an issue. We try to find input from the larger shareholders and if they decline to participate in this form then the nomination committee may not be aware of their views until committee has published its proposals. This is why we would prefer them to take part in the nomination committee so we could learn their views at that stage.

I understand that some foreign investors see it as incompliant with regulations to be an active owner in that way. We disagree, but that's up to each [investor]…. And they are right in the way that insider information might occur at this level and then you will be locked in for a period of time, but it's quite rare.

Conclusion

Shareholder committees provide stronger direct influence, at least for major shareholders, but may limit board and minority shareholder involvement. Their continued use in Iceland, Finland, Norway and Sweden reflects both historical governance practices and the ongoing influence of large shareholders in this region. The ultimate benefit of these distinct models depends on different shareholders’ priorities, and their ability to use voting rights and engagement with companies to ensure their interests are represented effectively.

Notes and References

1 Denmark is an outlier in the Nordic region, with most Danish companies utilizing board committees. The Danish Capital Markets act (“Lov om kapitalmarkeder”) stipulates that listed companies with a net turnover of DKK 100 million or more in two consecutive financial years must appoint a nominating committee consisting of members of the board; and the Danish Recommendations on Corporate Governance recommend that board committees consist only of members of the board and that the majority of members are classified as independent.

Danish Committee on Corporate Governance. Danish Recommendation on Corporate Governance. 2020. Section 3.4. https://corporategovernance.dk/sites/default/files/2023-08/Danish-recommendations-corporate-governance-02122020.pdf

2 The Finnish Corporate Governance Code recommends that either a board or a shareholder nominating committee is established to prepare proposals relating to the appointment and remuneration of the board of directors. Further, it is recommended that the majority of the members be independent of the company, and that members of the executive management not be appointed to the committee.

Securities Markets Association. Finnish Corporate Governance Code. 2024. Recommendation 18. https://www.cgfinland.fi/wp-content/uploads/2024/11/corporate-governance-code-2025.pdf

3 The Icelandic Financial Undertakings Act (“Lög um fjármálafyrirtæki nr. 161/2002”) stipulates that companies with a certain financial undertaking are to establish a nominating committee; and the Icelandic Guidelines on Corporate Governance include a section setting out the committee’s role.

Financial Undertakings Act. 2026. Article 53. https://www.althingi.is/lagas/nuna/2002161.html

4 The Norwegian Code of Practice for Corporate Governance states that companies should have a nominating committee which takes into account the interests of shareholders. The committee should be majority independent of the board and executive management and no members of the board and executive management are to serve on the nominating committee.

NUES. Norwegian Code of Practice for Corporate Governance. 2025. Section 7. https://nues.no/eierstyring-og-selskapsledelse-engelsk/

5 The Swedish Corporate Governance Code recommends that the nominating committee should have at least three members and be majority independent of the company and its executive management, with at least one member independent of the company’s largest shareholder. Members of the board can serve on the committee but should not constitute the majority. Members of the executive management should not serve on the committee.

Swedish Corporate Governance Board. Swedish Corporate Governance Code. 2024. Section III (2). https://bolagsstyrning.se/Userfiles/Koden/Dokument/SweCorpGovernanceCode_applicable_from_1_January_2024.pdf