Key Takeaways

On the Agenda is an interview series featuring Glass Lewis experts sharing their insights and perspectives on today’s governance, climate and stewardship issues facing institutional investors. On this occasion, Emil Moldovan, Head of Climate Science, sat down with Jermaine Reyes, Director, Content and Thought Leadership, to share his thoughts on the development process and methodology behind Glass Lewis’ Climate Intelligence Research.1

Emil’s expertise combines climate finance, supply chain, and AI, with a focus on its application for investors, by modeling company exposure to the climate mitigation economy. He holds a Masters in Environmental Science from Yale University.

On Timing and Market Demand

Jermaine Reyes: Thanks for taking the time to join us in conversation, Emil. So let’s get started. This spring, Glass Lewis launched its Climate Intelligence Research. As the Head of Climate Science, can you tell us why Glass Lewis is doing this now? And how this is different compared to what is already out there in the market?

Emil Moldovan: The market has shown new demand for climate signals that link to and integrate financial performance and outcomes. This goes beyond long-term risks, to also include ongoing costs, revenue opportunity, and overall profitability. Many of the frameworks, data, and current solutions out there display a disconnect between climate mitigation and financial performance. For example, the Science-Based Targets Initiative (SBTi) tracks pathways aligned with specific policy objectives, but it was not designed to evaluate company financial consequences over investment-relevant timeframes. Climate Intelligence Research connects the dots here, integrating both top-down scenarios, and bottom-up business activity analysis to provide systematic, comparable insights on how a lower greenhouse gas (GhG) economy can impact the bottom line.

Climate Intelligence Research also represents a departure for Glass Lewis, expanding our capabilities as an end-to-end stewardship services provider and demonstrating our human-centric approach to embedding AI and other new technology into research infrastructure. We’ve combined our analysts’ knowledge and expertise with our proprietary technology stack, and amplified that with a team of task-specific AI agents to scale our insights systematically across a large universe of companies. In addition to connecting human expertise with AI processing capacity, our infrastructure also has a robust governance layer to ensure the reliability and traceability of the intelligence.

On Valuation, Engagement and Portfolio Construction

JR: Climate Intelligence is built to primarily support investment research and engagement. Can you give concrete examples of how you have gone about structuring the insights to help investors in these areas?

EM: We are primarily targeting three use cases. The first one is company valuation. We provide a contextual background for investors who are trying to understand how the climate transition may impact the financial future of any one company. For example, we consider whether the company has assets that can enable their climate goals, or whether they have a revenue model that has been well thought out.

The second use case is engagement. All of our analyses conclude with a series of detailed conversation topics. These are not formal recommendations. Rather, they are open-ended points of consideration that highlight facets of a company's planning or execution – topics that investors may want to know more about and engage with management on. For example, we don't say, "The company should invest more in renewable energy." Instead, we may say, "We suggest clarifying the company's broad climate budget by specifying the exact amount allocated to renewable energy.”

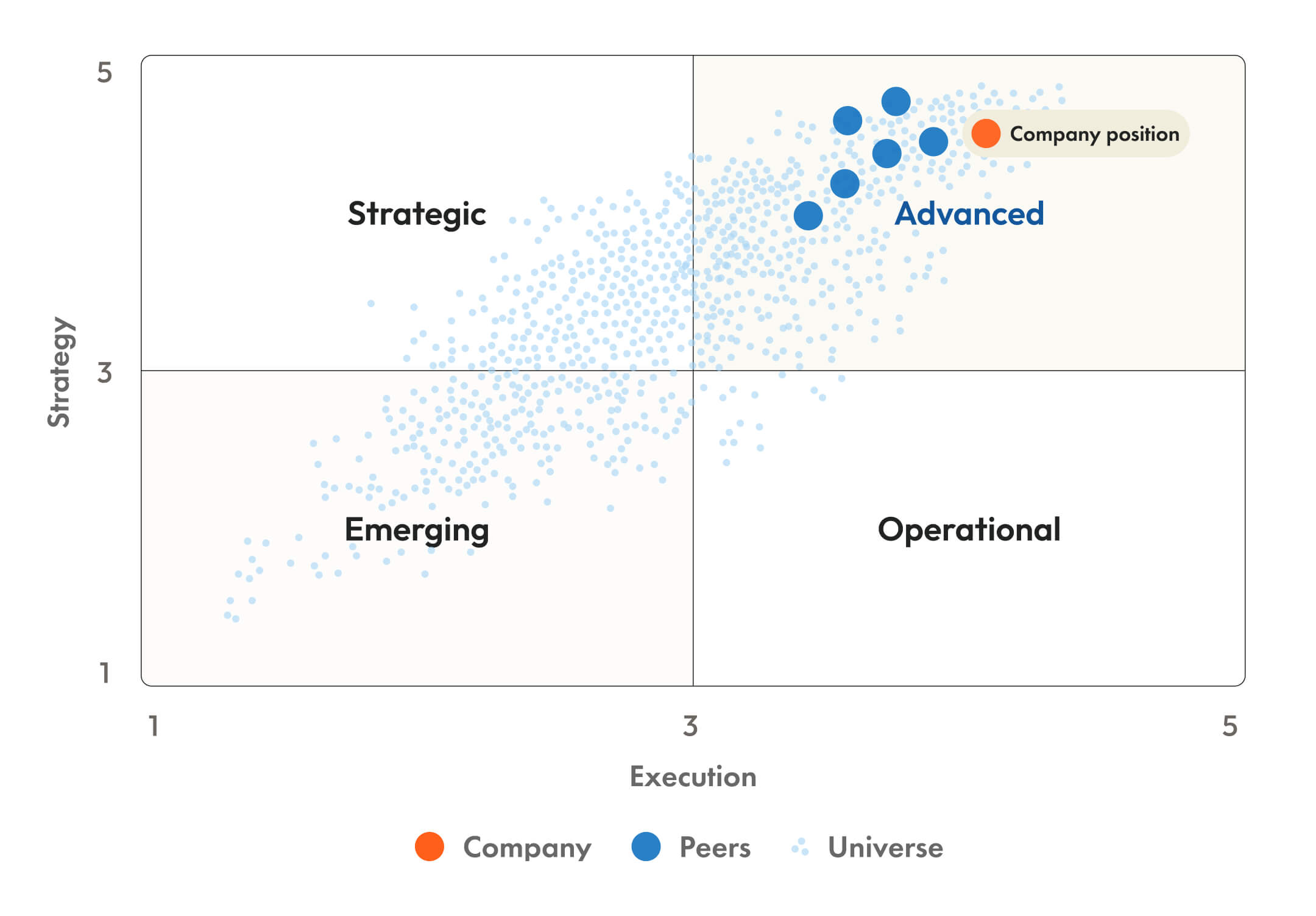

The third use case focuses on portfolio construction. And more specifically, the use case of comparing companies within and across sectors. Because our framework is standardized to a high degree, offering systematic insights across companies, investors can compare peers in terms of the materiality of various business activities, the maturity of their financial model, or their resourcing strengths.

On Methodology and Model Architecture

JR: In designing Climate Intelligence, what were some of the big directional choices you made in terms of the methodology and model architecture?

EM: Our methodology covers both downside exposure and upside potential, whereas many existing climate frameworks focus on risks. So we had to move beyond metrics such as value-at-risk (VAR) that do not do justice to potential upsides. This ended up being very important, as we recognized that in some sectors, certain companies are likely to be influenced mostly by risk and risk mitigation, while others are likely more exposed to opportunities relating to transition dynamics.

We also decided to base our methodological evaluation on financial materiality – a single materiality lens focused on how climate mitigation might impact a company’s financial performance and bottom line – not the company’s impact on the world, through, for example, GhG emissions. One consequence of this is that our methodology excludes company activities that are useful to reduce real world GhGs, but do not have a clear financial logic, such as the use of carbon credits. We only consider the impact of carbon credits on the company's financial position. Though they help companies hit their net zero goals, the link to real financial materiality is questionable. And, given the current overshoot trajectory, it’s also unclear to what degree capital markets, consumers, or regulators might “punish” companies not hitting net zero goals over time.

Another methodological choice we made is that the evaluation is future-oriented, with a five to seven-year investment-relevant time horizon. This led us to downplay a lot of the traditional metrics, such as GhG intensity based on carbon accounting, which speak to a company’s historical response. Measuring progress to date is important, but only insofar as it demonstrates the operational capability to continue making progress into the future. The extended horizon therefore means that signals relevant to short term fluctuations, such as commodity price forecasts one year out, are significantly downplayed, relative to the more structural drivers and transformations that companies are involved with.

On Transition Scenarios

JR: Transition scenarios are integrated into many climate data offerings, and can have significant impact on the outputs and signals derived from the research. How do you approach this with Climate Intelligence?

EM: We try to center our evaluation on what will lead to financial outcomes across multiple scenarios. For example, speaking loosely, reducing electricity usage through process efficiencies is financially wise 90% of the time, regardless of the policy regime, simply because energy will likely always be in demand as consumption continues to increase.

Our methodology incorporates proprietary scenarios, relying on assumptions that are realistic. We avoid implausibly sustainable scenarios, recognizing that even in the best circumstances, with interconnected economies, future developments are mostly incremental, where effecting real change takes time. And conversely, we don’t have a “very dirty” scenario because we see most major economies making significant moves on climate mitigation dynamics, despite what makes headlines in the news.

The decision to develop proprietary scenarios was made out of necessity. Most scenarios out there, for example, Network of Central Banks and Supervisors for Greening the Financial System (NGFS), Shared Socioeconomic Pathways (SSPs), and others, are solid, but don’t have the level of granularity that we need to forecast what will happen at the level of individual companies and their respective business activities. Further, they were not designed for equity evaluations. So, we rewrote our own scenarios based on standard practices; and we “downscaled” scenarios by articulating industry-specific consequences, which we then traced to the pressures that specific companies might be subject to.

On Challenges and Rewards

JR: What has been most challenging and rewarding with respect to building a fiduciary-grade research product like Climate Intelligence?

EM: The central challenge has been in balancing the need for company-level analysis rooted in very specific operational and business activities, with the need for scale across industries and indices. The rewarding part has been developing a framework which achieves that balance, measuring financial exposure to climate mitigation systematically across all of the sectors we cover.

We developed a way of standardizing the elements that scale across companies and simultaneously allowing variability from sector to sector and company to company. This means that while we use the same framework in all industries for all companies, we still evaluate each company based on its unique, financially material business activities, rather than a stereotyped reflection of what companies in a sector must do.

After lots of testing, we found that sweet spot of contrasting what is standard across industries versus what changes. And it has been rewarding to see the results: direct recognition of the elements that scale, and at the same time, deep company–specific insights that have allowed us to offer an apples-to-apples comparison across sectors, while providing depth relative to individual company contexts.

On Changes to Climate-Related Disclosures

JR: Thanks again Emil for sharing your in-depth insights. To wrap up, I'd like to ask one final question that exceeds our original five, but is quite pressing, given recent U.S. regulatory developments. With the SEC now proposing to rescind its climate-related disclosure rules and return to a more materiality-focused approach, how does this affect the product and the underlying research?

EM: Not much. Our assessments are not dependant on companies providing climate-specific disclosures. They certainly benefit from it, but it is not required as the framework focuses on financial materiality, which companies are required to report on either way. For example, if an industrial company has a large energy bill and they disclose it, that is enough for us. We know how to align that information with climate transition dynamics. It’s on us and our Climate Intelligence Research team to translate relevant financial disclosures and their consequences into a structured view of transition performance.

Notes and References

1 Each Glass Lewis product has its own proprietary methodology. The methodology discussed in this interview only applies to Climate Intelligence Research.

.jpg)