Climate Investing Redefined: Strategy and Execution as the New Lens to Understand Business Reality

Subscribe

Key Takeaways

- The financial impact of the climate transition on a company depends on how management interprets its specific climate risk–reward exposure across assets and markets, not just on top-down transition scenarios.

- A credible strategy is financially material, differentiated, and backed by real governance, clearly linking climate decisions to the core business model.

- Investors should look for aligned resources, delivery capability, and tangible financial results that prove strategy is translating into performance.

For investors considering how the low carbon transition impacts portfolio companies, a key challenge is understanding when and how it will affect valuations. With the transition moving from a long-term scenario to the nearer term, companies that face similar climate-related pressures have begun to diverge in how they respond.

Analysis of how the transition affects company value typically starts with downscaling macroeconomic scenarios, first to sector level and then to company level. These downscaled scenarios, in turn, provide the context for evaluating company specific information such as emissions, revenues and company disclosure on climate policies and risk management systems.

While in theory, this is the correct approach, in practice, it is hard to do. As we discussed in the first two articles in this series, bridging the gap between macro-scale and company-specific circumstances remains a challenge,1 exacerbated by a lack of relevant data and inconsistent reporting.2

In this article, we explore a different approach that enables investors to better understand the strategic reality as perceived in the boardroom and by company management. While transition scenarios remain an important input, we argue that long-term value creation ultimately depends on the choices made by an organization’s leadership in strategic planning and execution capacity.

Start With a Company’s Strategic Reality

Macroeconomic scenarios3 are valuable for understanding potential technological, consumer, or policy trends that companies will have to contend with. However, these scenarios only shape company outcomes indirectly, through how company management responds. As such, a better starting point for investment research is to listen to how leadership articulates the risk-reward landscape from their vantage point.

This landscape will be different for each company, depending on its portfolio of business activities and exposure to different markets. Scenario analysis, in turn, will help to better understand the transition risks and opportunities associated with its operations. For example, take a utility with both coal plants and a growing renewables business. The impact of the transition will differ across these activities. In a fast transition scenario, coal assets face early closures while renewables and grid investments accelerate; in a slower transition, coal generates cash flow for longer, but with higher long-term write-down risk, and clean energy growth is more gradual. From within a company, it is easier to see longer-term outlooks that are likely and how the company’s strengths or weaknesses set it up for viable pathways.

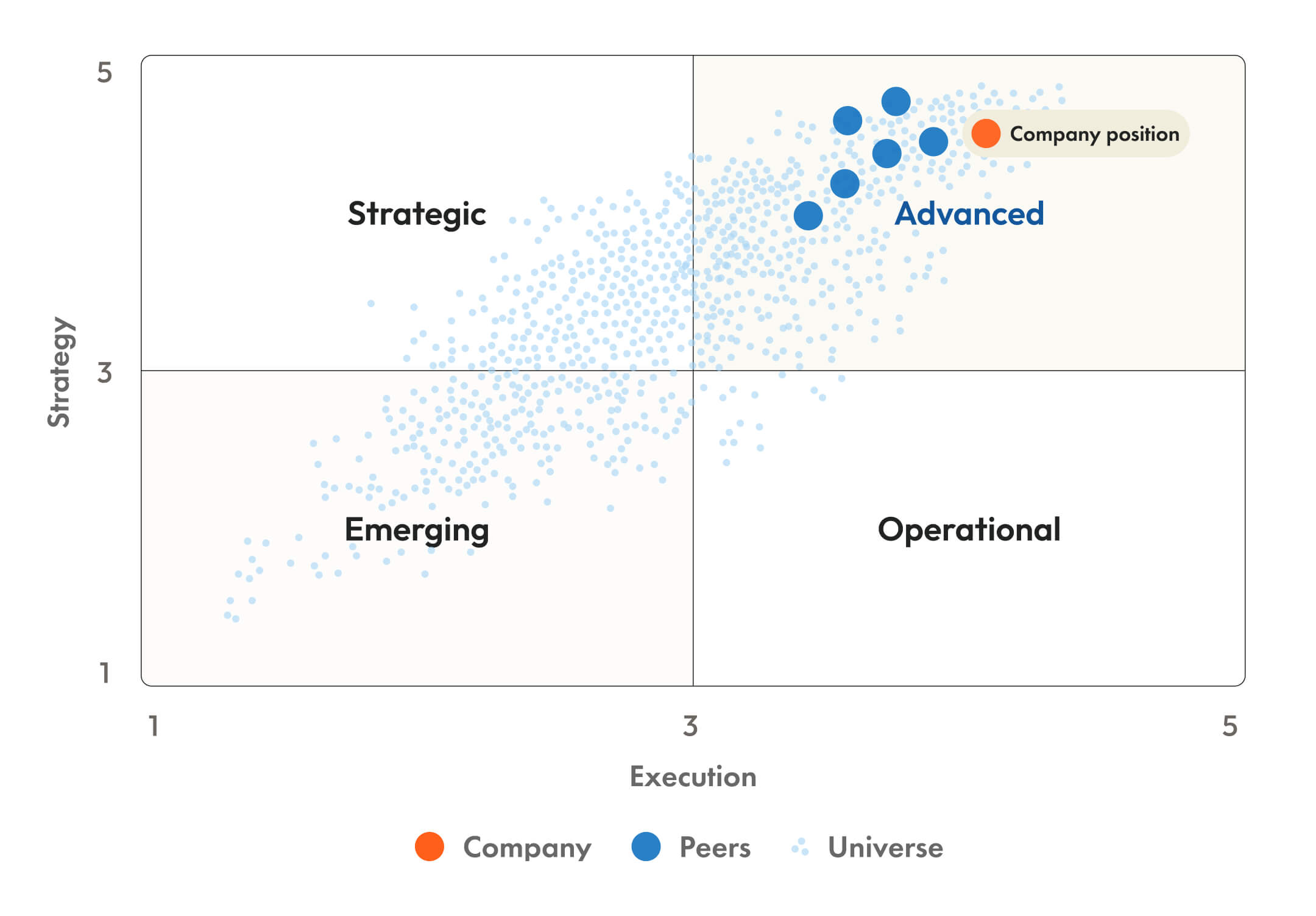

Analyze Both Strategy and Execution

The decisions management makes in response to its perceived risk-reward landscape can be divided into two broad categories: strategy and execution. Strategy is what the company says, while execution is what it does. These are conceptually distinct. A company can say one thing, and then not do it. Or, a company can execute without having articulated their strategy. The conceptual distinction is practically important, based on the time horizons in which climate mitigation is likely to influence company financial outcomes.

Consider an electronics manufacturer evaluating the use of recycled metals in its production. In the short term, execution drives outcomes: scrap metal may improve margins if the company is good at sourcing well-priced inputs. This is mostly an operational issue. Strategy becomes more relevant as management considers investments in scrap metal processing. It may take several years to deploy the capital, and several more for the ROI to materialize. On a very long time horizon, strategy starts to outweigh execution, potentially involving a broader shift in the business model.

On time horizons where both strategy and execution are important, investors may want to know about the divergences between the two. Consider a company with a complex new strategy that is not grounded in its manifest strengths. Investors may ask: is the strategy a bold transformation, or should we as shareholders intervene by asking management to explain whether goals are feasible? Consider also a company with execution competencies which it has not strategically framed as related to climate mitigation. This might be an opportunity for investors to have a conversation with management about, for example, entry into new markets.

The relative importance of strategy and execution will vary depending on the circumstances. But in each example, the strength of (and interplay between) these considerations serves as a through line from macroeconomic themes to company-specific outcomes, providing a window for investors to assess whether the company will deliver value.

Assessing the Strength of a Climate Strategy

A financially material climate strategy is a plan that shapes the company’s financial outcomes in an economy that values the reduction of greenhouse gases.

The foundation of a climate strategy is management’s perception of related risks and opportunities across its business portfolio. These can span many areas of the business, from energy procurement, material efficiency, consumer demand, to digitalization (and many others). In practice, companies often pursue multiple, overlapping strategies, many of which may not be explicitly labeled as “climate” initiatives.4 For investment research, this requires looking beyond stated climate disclosures to identify which strategic decisions are likely to be financially material under transition conditions. In the electronics manufacturing example, the use of scrap inputs may not be framed as climate strategy, but it can signal structural cost advantages or margin resilience, making it directly relevant for earnings forecasts.

Governance is a critical filter: a climate strategy that is overseen by the CEO, CFO, and board is more likely to be reflected in capital allocation decisions and financial planning. For investors, this provides a basis to evaluate whether climate decisions are grounded in leadership experience and embedded in mandates and incentive structures or remain peripheral. From a stewardship perspective, weak governance signals, such as limited board oversight or lack of financial accountability, create a clear entry point for engagement.

Assessing the strength of a strategy also requires evaluating its internal logic and competitive positioning. There are many things to consider here: how do companies determine pathways and maintain optionality? Does the strategy appear feasible — for example, is it evidenced by awareness of dependencies and risks? Does the strategy differentiate the company from competition? These questions map directly to investor concerns. A strategy that credibly lowers cost of goods sold, expands into new markets, or strengthens pricing power should feed into forward-looking margin and growth assumptions. In the working example, investors would assess whether the use of scrap metal can deliver a sustained cost advantage relative to peers, informing both relative valuation and position sizing.

Where gaps emerge, such as a strategy that lacks feasibility or is not supported by governance decisions, investors can engage management to challenge the choices made or contrast them with peer examples. In this way, analyzing climate strategy is not only a tool for forecasting outcomes, but also a basis for targeted, financially grounded stewardship.

Evaluating Execution Capacity

If strategy defines what a company intends to pursue, execution is the operational path from intent to financial result. The path to solid execution runs through various requirements, where each step builds on the last. For investors, this is where climate considerations become observable in capital decisions and financial outcomes.

Execution on climate strategy starts with resources. These include the right assets, talent, supply chain access, market positioning, and capital. A strong resource base gives the company options that are difficult for competitors to replicate, while a thin one limits the scope of what management can realistically deliver. Resources might not be interchangeable. A gap in any single resource may constrain what companies can deliver. For investment research, this provides a practical lens to assess whether stated strategies can be supported by the company’s existing capabilities. Weak or misaligned resources may signal a higher likelihood of delays, cost overruns, or under-delivery, which can be reflected in more conservative forecasts. The flow of capital toward vetted projects — that have clear links to strategic priorities — indicates that resources are being leveraged with intention.

Resources, however, do not create value until they are mobilized. Organizational capacity determines whether a company can translate its resource base into sustained delivery, particularly for complex, multi-year initiatives. From a stewardship perspective, limited evidence of coordination, accountability, or delivery track record provides a basis for engagement focusing on how management plans to operationalize strategy and whether the organization is equipped to execute at scale.

Financial performance ultimately validates whether this execution path was successful or fell short. Financially material climate strategies should surface in the financials through new revenue opportunities, efficiency gains, or cost reduction. If these signals are present, they suggest that the resource base was adequate, that the company’s management activated it, and that investment was well directed. For investors, these outcomes inform earnings forecasts, returns, and valuation. Where expected financial signals fail to materialize, investors have a basis to reassess assumptions or to engage management on delivery gaps.

Strategy and Execution for Continued Value

The fundamental challenge for investors remains in closing the gap between macro-level climate trends and micro-level company valuations. While high-level scenarios indicate the direction of the global economy under the low carbon transition, they offer limited insight into which specific firms will perform well in the shift. We believe it is possible to bridge this divide, not by grading a company’s stated intentions, but by pressure-testing both the logic of their strategy and their ability to execute.

To summarize, on the strategy side, the key question is whether management has moved beyond generic pledges to identify a differentiated path that is relevant to their business model. We look for a strategy that doesn't just react to the transition, but proactively shapes a competitive advantage within it. On the execution side, the focus is on delivery and friction. We look for a resource moat, such as specialized talent, physical assets, and supply chain depth, that demonstrates that a company is retooling its industrial engine rather than just managing its reputation.

While these measurements are not crystal balls, they reveal the business logic of a company’s climate transition. For investors, the ability to decode these signals is the difference between speculating on the possible impacts of macro trends and identifying the individual companies best prepared to deliver value.

Notes and References

1 Moldovan, E., Timmer, D. “Translating Climate Science Into Investment Decisions.” Glass Lewis. December 2, 2024. https://www.glasslewis.com/article/translating-climate-science-into-investment-decisions.

2 Moldovan, E., Timmer, D. “The Climate Intelligence Landscape: Current Limitations and the Road to Improved Financial Signals.” Glass Lewis. January 7, 2026. https://www.glasslewis.com/article/climate-intelligence-landscape-current-limitations-road-improved-financial-signals.

3 O’Neill, Brian C., Elmar Kriegler, Kristie L. Ebi, Eric Kemp-Benedict, Keywan Riahi, Dale S. Rothman, Bas J. Van Ruijven et al. "The roads ahead: Narratives for shared socioeconomic pathways describing world futures in the 21st century." Global environmental change 42 (2017): 169-180.

4 For example, their approach to energy costs, or AI, or onshoring.

.jpg)