.jpg)

Key Takeaways

- On a recent webinar, Proxinvest analysts shared data and findings on how CAC 40 companies incorporate ESG criteria into executive compensation.

- All CAC 40 companies include at least one ESG metric in their executive incentives, and 70% incorporate ESG in both their annual bonus and their LTI.

- Quantitative metrics were far more common than qualitative or discretionary measures, representing 73% of the ESG criteria used in annual bonuses and 97% of those included in LTIs.

- Over three-quarters of the ESG criteria in variable remuneration focused on environmental and social performance, and the most commonly used metrics were reduction of greenhouse gas emissions, diversity, and CSR strategy.

- Slightly more than half the time, the actual ESG-related payout was lower than the theoretical metric weighting, reflecting underperformance relative to targets.

For investors, incorporating environmental, social and governance (ESG) criteria into executive compensation is a key consideration, as the variable pay structure is viewed as an effective lever for driving change within companies. This article provides data and analysis of how French listed companies on the CAC 40 integrated ESG into their variable pay structures in 2025.1

ESG Metrics in Variable Compensation

Our study shows that all CAC 40 companies include at least one ESG metric in either executives’ annual bonus or long-term incentive (LTI) plan. In addition, 70% of these companies incorporate ESG in both their annual bonus and their LTI.

Figure 1. CAC 40 ESG Metric Use by Plan Type

.png)

Source: Proxinvest Research.

With regard to the nature of the ESG metrics used in CAC 40 remuneration, a large majority are quantitative. Quantitative metrics represent 73% of the ESG criteria used in annual bonuses and 97% of those included in LTIs. We also observed that most ESG metrics are internal, meaning they do not require peer comparison or rely on ratings provided by external organizations.

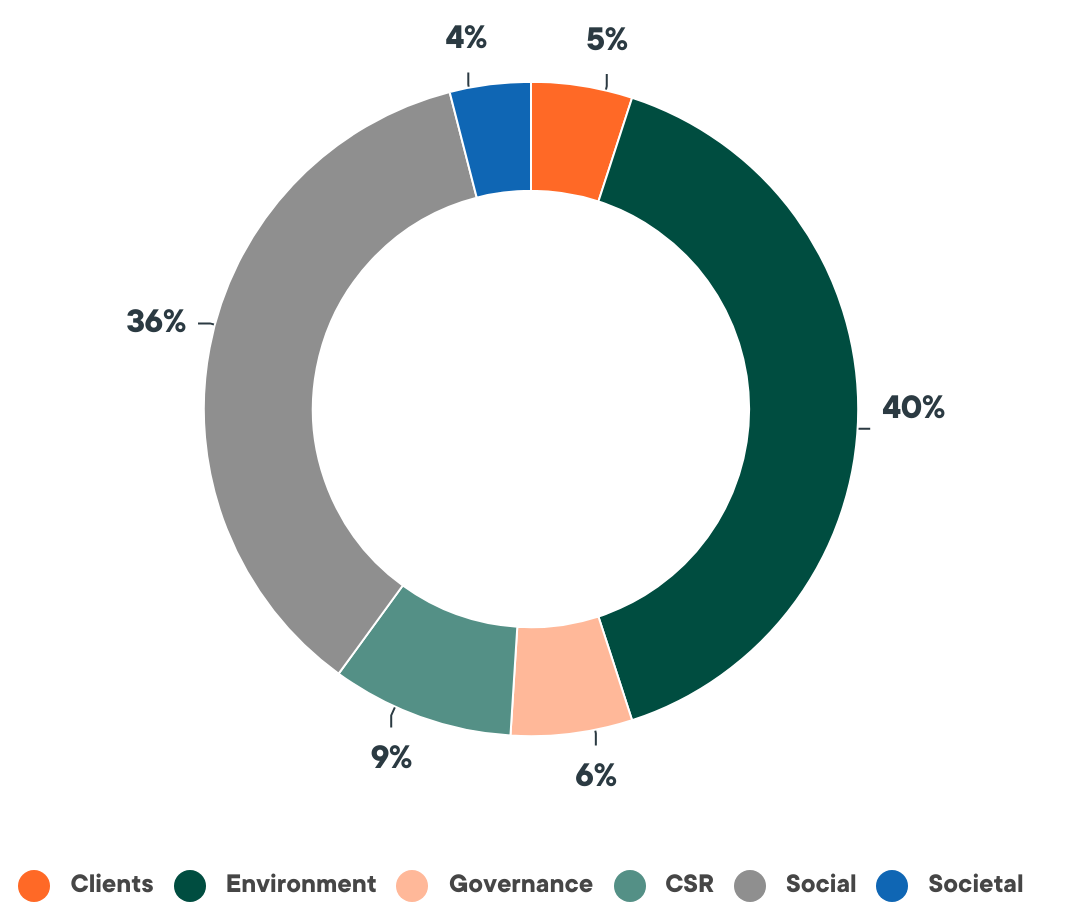

Distribution of ESG Categories

We identified six categories of ESG criteria.2 Among these, the environment and social categories stand out, representing 40% and 36% of ESG metrics included in variable remuneration, respectively (Figure 2). The least represented category relates to societal metrics, which account for only 4%.

Figure 2. CAC40 ESG Criteria by Category

Source: Proxinvest research.

Other notable findings include:

- Environmental and social metrics are the most widely used across all sectors.

- In the energy sector, environmental metrics account for up to 70% of ESG criteria.

- In the telecommunications services sector, social metrics represent more than 60% of ESG criteria.

- Societal metrics appear in only four sectors: pharmaceuticals, biotechnology & life sciences, banks, utilities, and food, beverage & tobacco.

As part of our study, we compared the theoretical weighting of ESG metrics (i.e., as disclosed in remuneration policies) with their actual weight in annual bonus payouts. Although all CAC 40 companies disclose the theoretical weight of ESG metrics, not all disclose details of the actual performance achieved, which makes it impossible in some cases to determine what proportion of payouts were based on ESG performance.

Among companies with sufficient disclosure, the actual ESG payout exceeded the theoretical weighting in 40% of cases, indicating that performance targets were surpassed. Conversely, in 53% of cases, the actual ESG payout was lower than the theoretical weighting, reflecting underperformance relative to targets.

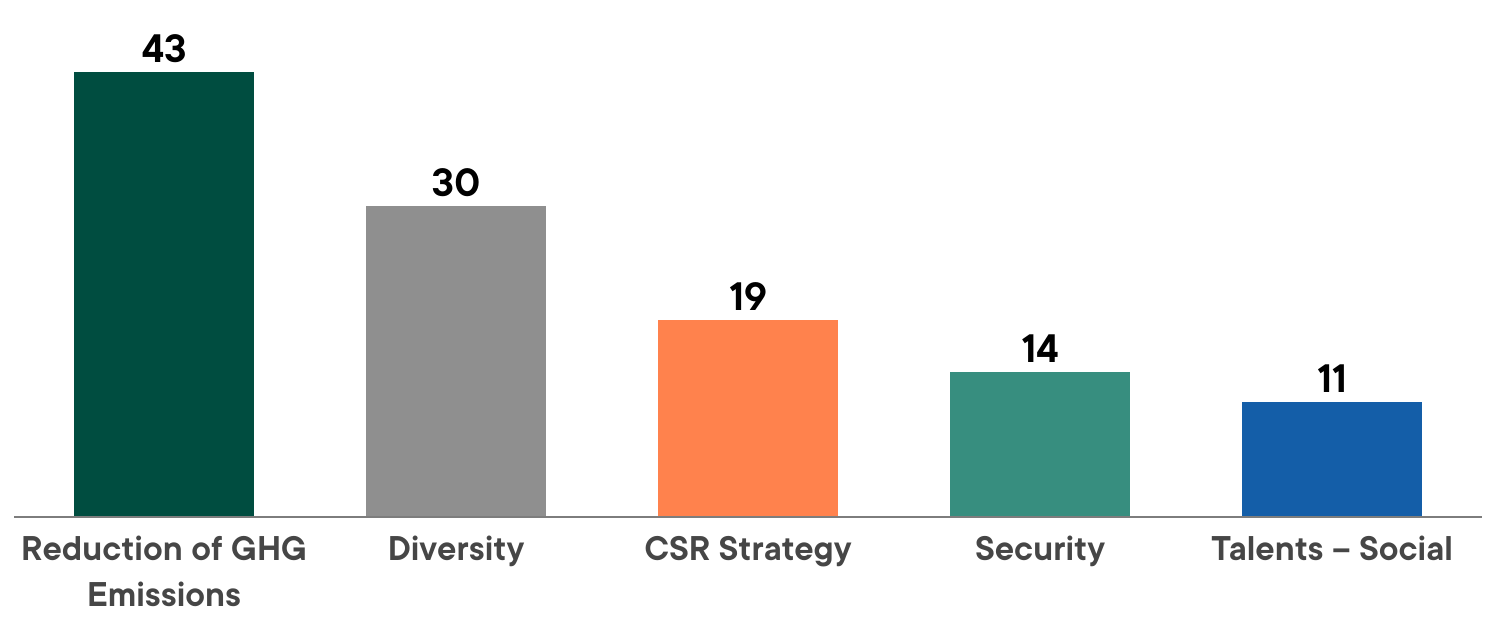

Types of ESG Metrics and Their Frequency

In total, we identified 36 distinct types of ESG performance measures. The most frequently used are: reduction of greenhouse gas emissions, diversity, and corporate social responsibility (CSR) strategy.

Figure 3. Top 5 Most Commonly Used ESG Metrics at CAC40 Companies

Source: Proxinvest Research.

Our analysis reveals a lack of correlation between how frequently a metric is used and its theoretical weight. For example, the reduction of greenhouse gas emissions is the most commonly used metric, yet its average theoretical weight is among the lowest (7.27%). Conversely, CSR strategy is used less frequently, but carries a relatively high theoretical weight.

This discrepancy can be explained by the nature of CSR strategy, which often refers to broad roadmaps encompassing multiple indicators, such as improving diversity, reducing accident rates, or lowering carbon emissions. Instead of assigning separate ESG metrics with smaller weights, companies may choose to consolidate several objectives into a single, broader criterion with a higher overall weight.

The ESG Factor Versus Individual Metrics

Looking beyond the CAC 40 to SBF 80 and Euro Stoxx 50 companies, we identified a practice that remains limited in use, but has significant impact: the ESG factor. Under this approach, ESG is not treated as a standalone, weighted metric that determines a specific portion of the potential payout. Instead, it acts as a multiplier applied to the overall variable remuneration. As a result, its impact is greater than that of a single ESG metric.

We identified eight companies using an ESG factor. These ESG factors generally rely on a narrower range of criteria than traditional variable remuneration frameworks and are primarily based on environmental indicators.

Conclusion

In examining how French companies incorporate ESG criteria into executives’ variable remuneration, we observed a variety of approaches. Companies measure a range of different types of ESG performance, with certain criteria more popular in certain sectors. The time-frame of short- and long-term incentives is also a factor, influencing both choice of metric and the importance of how those metrics are weighted. Some companies avoid weighting entirely, instead using an ESG multiplier approach that can have a strong impact on overall payouts.

While each company’s approach will reflect its specific circumstances, we also identified some common practices throughout the market. Out of six categories of ESG criteria, environmental and social are by far the most common (76%), and in most cases, variable compensation relies mainly on internal, quantitative and verifiable metrics. Overall, the integration of ESG metrics is widespread across the CAC 40, typically influencing both short- and long-term incentives.

Notes and References

1 Based in Paris, Proxinvest provides in-depth local proxy research and analysis, and for 25 years has published an in-depth annual review of SBF 120 executive remuneration. The full report is published and shared with clients as Proxinvest. "La Rémunération des Dirigeants des sociétés cotées françaises". November 18, 2025. In early February 2026, Proxinvest held a webinar for its institutional clients on ESG Criteria in the Compensation of CAC 40 Executives, on which this article is based.

2 The six criteria identified are: 1) Customers: covers criteria relating to customers in general. 2) Environment: refers to criteria relating to environmental protection, sustainable development, renewable energy and associated regulatory aspects. 3) Governance: refers to criteria relating to company directors, their succession, and regulatory aspects relating to their roles. 4) Social: refers to criteria relating to company employees. 5) Societal: refers to criteria relating to the company's impact on society at large. 6) CSR: this is a generic category that includes criteria that either fell under different categories or were not sufficiently described by companies.

.png)