How Plurality Voting Allows Directors to Stay on the Board Without Majority Support

Subscribe

Key Takeaways

- Out of the 22,635 U.S. director election proposals Glass Lewis covered in the 2025 proxy season, there were 72 directors from 48 different companies who did not receive majority shareholder support.

- Of those 72, only seven successfully resigned. Six had their resignations rejected and the remaining companies took no action, instead ignoring the vote outcome and letting the directors continue to serve despite not receiving majority shareholder support.

- These majority-unsupported directors stay on due largely to plurality voting, which removes the possibility of failing to be elected, so long as there are uncontested board seats available.

- In 2025, 50 of the 72 majority-unsupported directors, or 69.4% of total, served on boards that use plurality voting and do not require a resignation policy for uncontested director elections.

- Negative governance practices insulate boards from shareholder concerns. In 2025, 39.6% of companies with majority-unsupported directors had a classified board, and 12.5% had a multi-class share structure.

The tendency for directors who did not receive majority shareholder support to remain on their boards is a longstanding and unique feature of the U.S. market. While the number of majority-unsupported elections in the U.S. has decreased over the last two years, most of these directors continue to retain their board seats, often without public disclosure acknowledging the majority opposition or shareholder engagement addressing what caused it.

This lack of responsiveness is largely driven by the continued prevalence of plurality voting standards, where nominees receiving the most “for” votes are elected to the board regardless of whether they receive majority support. And it is perpetuated by the presence of negative governance features such as classified boards and multi-class share structures, which both lead to, and insulate directors from, shareholder opposition.

This article examines trends in recent U.S. voting data, looking at the drivers and implications of majority-unsupported directors, with a focus on the use of plurality voting and governance practices that undermine board accountability.

The Prevalence of Majority-Unsupported Directors

Directors that receive less than majority support (i.e., less than 50% of votes cast in favor of their election) are relatively rare, with nearly 84.5% of nominees in proxy season 2025 (83% in 2024; 80.9% in 2023) receiving greater than 91% shareholder support.1 Out of the 22,635 director election proposals in our U.S. coverage during the 2025 proxy season, there were 72 such directors (69 directors in 2024; 93 directors in 2023) from 48 different companies. Of those directors, only seven successfully resigned (nine directors in 2024; 11 directors in 2023). Six had their resignations rejected (nine directors in 2024; 13 directors in 2023) and the remaining companies took no action, instead simply ignoring the vote outcome.2 Notably, 33 (45.8%) of these directors were from companies in the Russell 3000 (39 in 2024; 39 in 2023) and from these companies, only one director successfully resigned (six directors in 2024; 2 directors in 2023), while five directors had their resignations rejected (seven directors in 2024; seven directors in 2023).3

Figure 1. Majority-Unsupported Directors in U.S. Coverage, Proxy Season 2025

Source: Glass Lewis Research. Data as of the 2025 proxy season period of Jan. 1 to June 30, 2025.

While the number of majority-unsupported directors across our full coverage increased slightly, the number of rejected resignations continues to decrease, a trend we have observed over the past several years. In addition, the overall number of these directors within the Russell 3000 experienced a notable decrease (15.4% decrease) compared to the past two years.

Drivers of Director Opposition and Their Implications

The continued service of majority-unsupported directors on companies’ boards is often a symptom of underlying governance concerns. In addition to the governance issues driving the voting opposition, their continued presence indicates a lack of board accountability and responsiveness to shareholder concerns. These concerns are exacerbated when companies fail to provide disclosure addressing the opposition.

In the 2025 season, the top five most common drivers of majority opposition included concerns relating to board gender diversity (18%), poor responsiveness to prior shareholder opposition (15%), director attendance (13%), excessive director commitments (13%) and multi-class share structures with unequal voting rights (11%), among other concerns.4 Notably, individual director concerns, such as attendance and director commitments, increased as significant drivers of majority opposition, indicating that shareholders may be placing greater scrutiny on directors’ abilities to fulfill their fundamental duties to shareholders.

Figure 2. Most Common Drivers of U.S. Majority Director Opposition in 2025

.png)

Source: Glass Lewis Research. Data as of the 2025 proxy season period of Jan. 1 to June 30, 2025.

In addition, majority-unsupported directors often serve on boards with other negative governance practices, such as classified boards,5 that both drive shareholder opposition and serve to shield directors from that opposition. In 2025, six of the 48 companies with majority-unsupported directors (12.5%) maintained a multi-class share structure (4.9% decrease from 2024) and 19 companies (39.6%) maintained a classified board (14.7% decrease from 2024).6

Majority Opposition Declines as Governance Practices Improve

There are several possible explanations for the recent decreases in the number of directors who do not receive majority support, both at companies with negative governance practices and overall. Notably, the decline appears to align with a trend of companies taking gradual steps to address the concerns raised by shareholder voting, and to improve their governance practices more broadly.

For example, in recent years a significant number of companies have responded to overcommitment concerns by implementing director commitments policies.7 Similarly, average board gender diversity for the Russell 3000 has increased by nearly 4% since 2023, to 30.6%.8 Over the same period, the number of directors whose failure to receive majority support likely stemmed from gender diversity concerns has decreased from 21 in 2023 to 10 in 2025.

Notably, seven of the ten elections in 2025 where board gender diversity was a driver of majority opposition served at companies with a classified board and/or multi-class share structure, again highlighting the impact of negative governance practices. Some companies are taking steps to eliminate structural restrictions on shareholder agency. In the 2025 proxy season we observed an increase in bylaw amendments seeking the elimination of supermajority provisions (70.6% increase), repeal of classified boards (36.2% increase), and adoption of special meeting rights (47.1% increase), among others.

Steps for Promoting Board Accountability

When directors receive high levels of shareholder opposition, board responsiveness is crucial. In these circumstances, and particularly when a director does not receive majority support, it is generally viewed as market best practice for companies to engage with shareholders, provide robust disclosures surrounding their engagement efforts, and communicate the measures they are taking to address underlying concerns in their proxy filings.

Shareholder engagement is an effective tool that promotes constructive feedback and an open dialogue. It provides issuers with the opportunity to gain insights into the primary drivers of the opposition and find ways to resolve or mitigate shareholder concerns. Disclosures surrounding shareholder engagement and the related measures taken further demonstrate responsiveness and may bolster investors’ confidence in the board. If a director has submitted their resignation in response to low shareholder support, disclosure of the rationale surrounding the board’s decision to accept or reject the resignation is another important consideration.

When majority-unsupported directors remain on the board, shareholder engagement coupled with increased disclosure serves to acknowledge shareholder concerns, while giving boards the occasion to provide an adequate and thoughtful response, helping to support long-term shareholder value.

The Problem With Plurality Voting

Although multi-class share structures, classified boards, and poor board responsiveness all contribute to voting opposition, the primary perpetrator for the continuation of majority-unsupported directors on U.S. boards is plurality voting.9 Under plurality voting, director nominees receiving the most “for” votes are elected to the board until all available board seats are filled, regardless of whether those nominees receive a majority of votes cast in favor of their election. This means that in an uncontested election, a director could, in theory, be elected by a single “for” vote, removing the possibility of “failure” so long as there are uncontested board seats available.

Although shareholders may “withhold” their votes from directors, this option serves only as a symbolic means of communicating disapproval of a candidate. As a result, directors receiving a greater number of “withhold” votes than “for” votes may still be elected to the board. This further demonstrates how plurality voting may diminish shareholder voices when compared to majority voting, where uncontested nominees are only elected to the board when they receive a higher number of votes cast "for" than the number of votes cast "against." Furthermore, because majority support is technically not a consideration in plurality voting, companies often fail to provide disclosure pertaining to directors who do not receive majority support.

Companies may choose to implement resignation policies in conjunction with their plurality voting standards, requiring directors who receive a greater number of “withhold” votes than “for” votes to submit a letter of resignation to the company’s board and/or nominating and corporate governance committee for consideration, which can then be approved or rejected by the board. Applying a resignation policy introduces a level of accountability to the board, encouraging boards to address shareholder concerns and the continued service of an unpopular director.

However, even where a resignation policy is in place, the board retains the right to reject a director’s resignation, despite majority shareholder opposition. In practice, the vast majority of director resignations are subsequently rejected by the board. True majority is the only voting standard that forces directors to stand down upon receiving majority opposition, granting shareholders the ultimate authority, while disallowing boards’ from rejecting director resignations.

Plurality Voting and Majority-Unsupported Directors in 2025

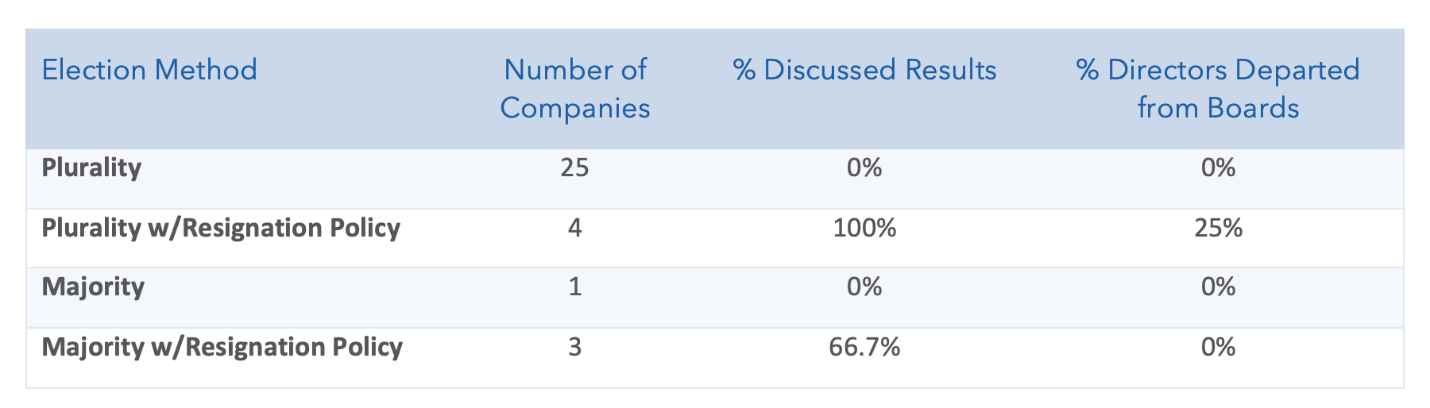

Among the 72 majority-unsupported directors in the 2025 proxy season, 50 (from 35 different companies) served on boards with plurality voting (without a resignation policy for uncontested director elections), representing about 69.4% of total.

Although most S&P 500 companies have adopted majority voting, plurality voting remains the default standard for uncontested director elections at most U.S. mid-cap and small-cap companies. Across our total U.S. coverage, 1,882 companies (48.8%) use plurality voting in uncontested director elections, with 999 of these companies in the Russell 3000 (representing 25.9% of the index) and 22 in the S&P 500 (approximately 0.6%). Comparably, only 303 companies within our overall coverage (7.9%) use plurality voting with a resignation policy requiring directors to tender their resignation if they do not receive majority shareholder support.

Figure 3. Election Methods at Russell 3000 Companies With Majority-Unsupported Directors, 2025

Source: Glass Lewis Research. Data as of the 2025 proxy season period of Jan. 1 to June 30, 2025.

It is worth noting that while the overall number of majority-unsupported elections is trending downward, the number of companies with both majority-unsupported directors and plurality voting has steadily increased since 2023, further underscoring the role that plurality voting plays in keeping many unpopular directors on U.S. boards.

Looking Ahead

Despite a recent decline in the number of majority-unsupported director elections in the U.S. market, the low proportion of these directors that actually leave the board remains a concern. In many cases, their presence can be seen as a catch-22, driven by negative governance practices such as multi-class share structures and classified boards that insulate directors from shareholder opposition.

Recent efforts by companies to improve their governance practices suggest that increasing the degree of board accountability to shareholders is possible – however, the cycle of majority-unsupported directors looks unlikely to end until the U.S. market shifts away from plurality voting standards, and towards majority voting.

Notes and References

1 Glass Lewis. U.S. Proxy Season Review 2025.

2 Ibid.

3 Ibid.

4 Ibid.

5 A classified (or staggered) board of directors consists of members divided into different classes who serve overlapping, multi-year terms, where only a fraction of the board is elected each year.

6 Ibid.

7 Nolledo, S. “A Review of Director Commitments Policies, 2023 to 2024.” Glass Lewis. January 23, 2025. https://www.glasslewis.com/article/a-review-of-director-commitments-policies-2023-to-2024.

8 Glass Lewis. U.S. Market Snapshot 2025: Board, Governance & Disclosure.

9 Glass Lewis. Market Overview: U.S. Election of Directors Voting Standards. 2025. Accessed January 10, 2026.