Make Whole Awards, Retention Grants, and the Rising Costs of Executive Recruitment

Subscribe

Key Takeaways

- Executive sign-on and retention grants made up over 60% of all “one-time” awards among S&P 500 companies in proxy season 2025.

- The average value of both sign-on and retention awards among S&P 500 companies jumped significantly from proxy season 2024 to 2025, by 40% and 63% respectively.

- A majority of these sign-on awards included “make-whole” considerations, to compensate an executive for amounts forfeited from the prior employer.

- On average, make-whole grants were larger than sign-ons overall ($4.6 million, vs $3.5 million), making up 70% of the value of all S&P 500 sign-on awards.

- Investors and non-investors have different expectations for the disclosure and treatment of make-whole awards.

The need for strong leadership amid a perceived scarcity of executive talent is raising the stakes for recruitment, retention and succession planning.1 With boards trying to either ensure a smooth transition, or avoid an unnecessary one, the average value of both sign-on and retention awards grew significantly from 2024 to 2025 among S&P 500 companies.2 This escalating cycle is nothing new. But it is being accelerated by the increasing prevalence of “make-whole” awards, granted to compensate executives for pay amounts forfeited by leaving their previous employer.

This article presents data on U.S. companies’ use of executive sign-on and retention grants, and examines an apparent divergence in how investors and non-investors view the awards.

Prevalence of Succession-Related One-Off Awards

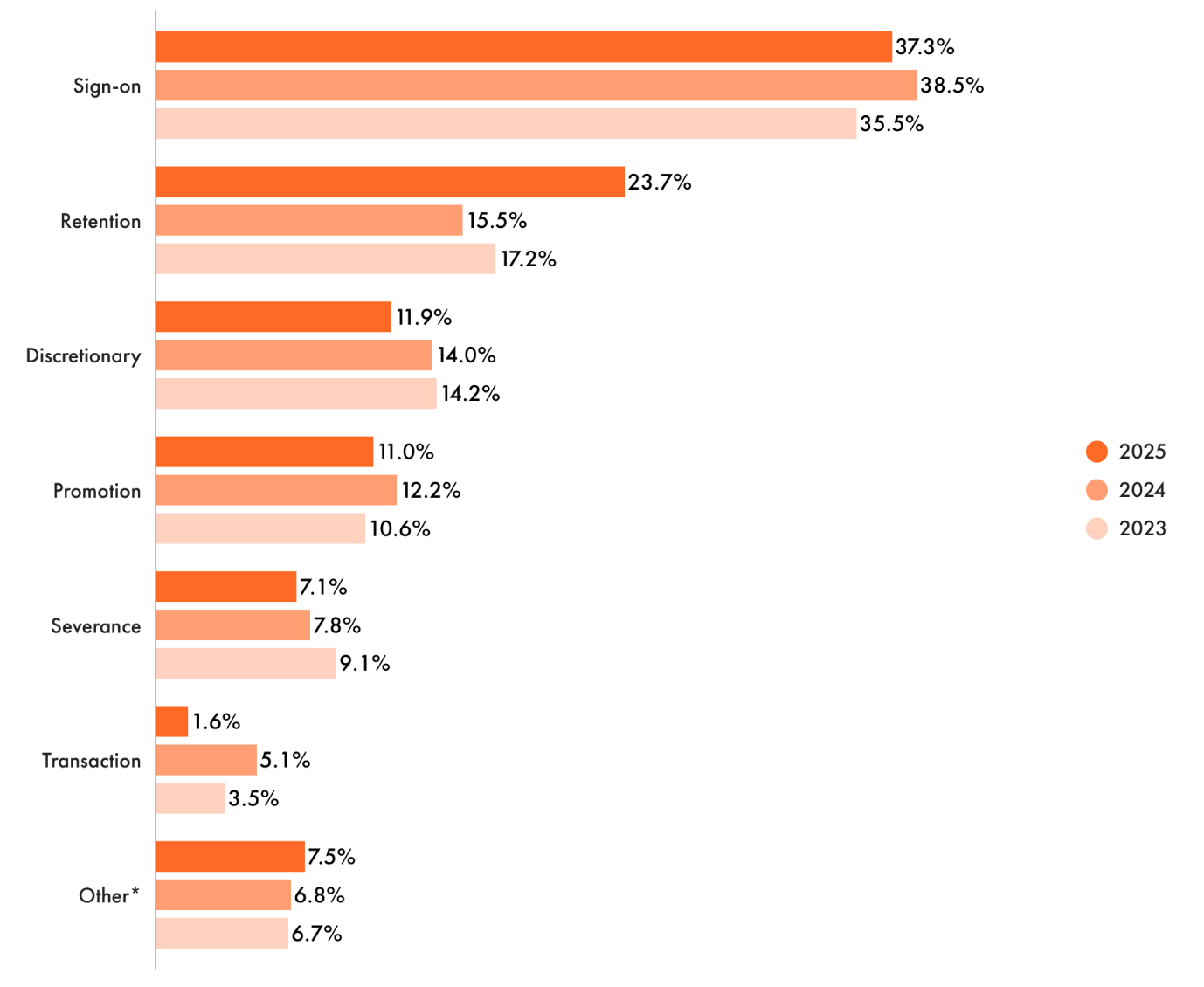

Sign-on awards continued to be the most prevalent type of one-time award among S&P 500 companies (Figure 1), with over one-third of all one-time awards granted in each of the past three years being classified as sign-on.3

Figure 1. Types of One-Time Awards Among S&P 500 Companies

Source: Glass Lewis Research. Data as of the 2025 proxy season period of Jan. 1 to June 30, 2025. Note: “Other” includes employment agreement awards, grants for service as an interim executive, guaranteed bonuses and awards that do not otherwise fall in one of the other categories.

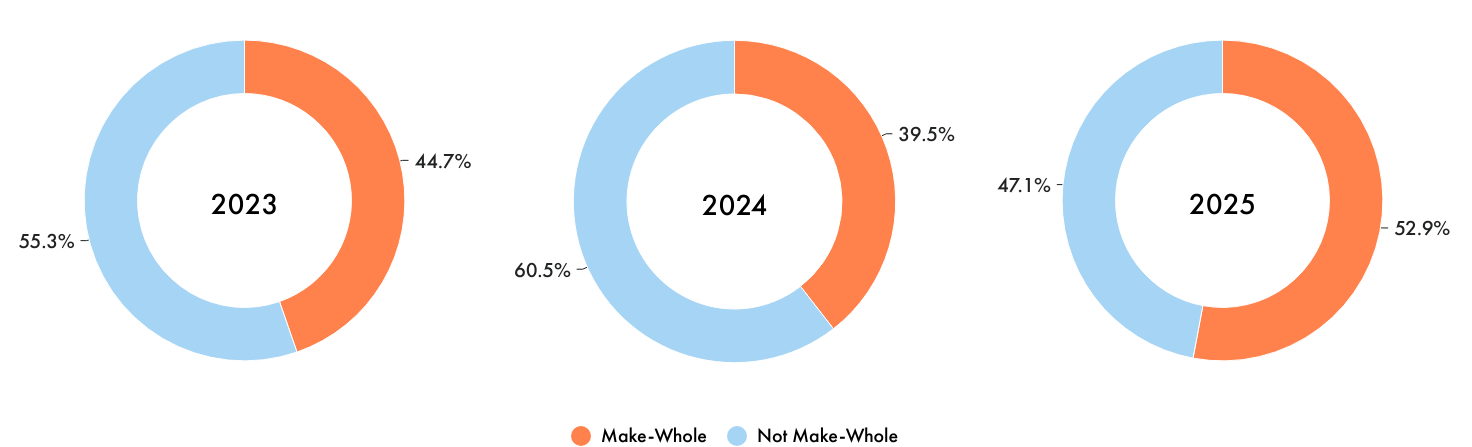

In 2025, the percentage of sign-on awards where companies disclosed make-whole considerations as a rationale, at least in part, made up a majority of sign-on awards granted (Figure 2). This followed a decline in the disclosure of make-whole considerations in 2024. The average value of sign-on awards in the S&P 500 appears to be positively correlated to the number that include make-whole considerations, with the average sign-on award reported in 2025 being $3.5 million, a rebound from the decline in value from 2023 to 2024 (2023: $3.3 million; 2024: $2.5 million).4

Figure 2. Use of Make-Whole Considerations for S&P 500 Sign-on Awards

Source: Glass Lewis Research. Data as of the 2025 proxy season period of Jan. 1 to June 30, 2025.

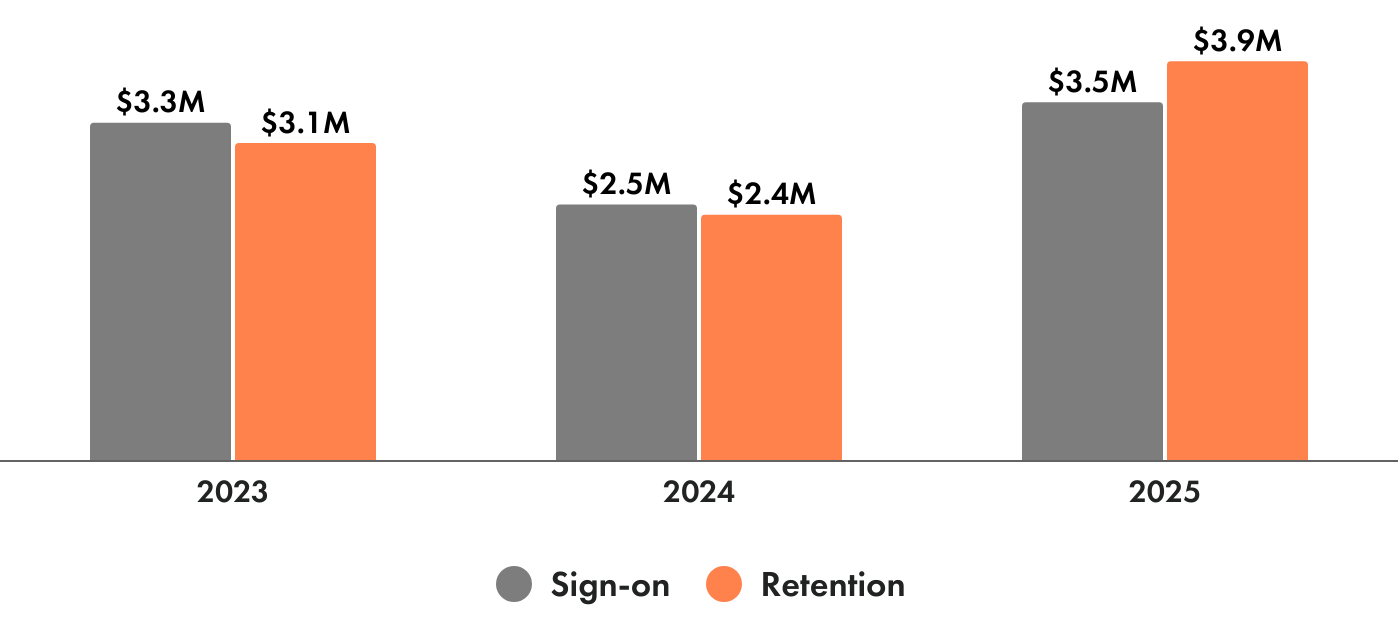

Companies often list concerns around the poaching of executives as a rationale for retention awards. Given this context, it is notable that following the drop in the average value of a retention award in the S&P 500 during the 2024 proxy season (2024: $2.4 million; 2023: $3.1 million), 2025 saw a substantial jump to $3.9 million (see Figure 3). The 61% jump in value mirrors a similar rise in the value of retention awards in the years following the outbreak of the COVID-19 pandemic, where the value increased approximately 57% from 2019 to 2021. Considering the above, the increases in the value of retention awards may provide further upward pressure on sign-on award values.5

Figure 3. Average Value of S&P 500 Retention and Sign-on Awards

Source: Glass Lewis Research. Data as of the 2025 proxy season period of Jan. 1 to June 30, 2025.

Make-Whole and Retention Grants for Executive Officers

During the 2025 proxy season, Glass Lewis’ quantitative analysis covered 204 CEO transitions among U.S. companies, a decrease from 223 in the prior season. While the number of CEO transitions decreased, the value of awards granted in connection with named executive officer (NEO)6 transitions increased, especially for S&P 500 companies. This suggests that more transitions are relying on hiring external candidates, as more one-off grants are expected for these appointments compared to internal promotions.

One major reason for this trend is the increasing prevalence of make-whole sign-on awards for new NEOs. Of the awards reviewed during the 2025 proxy season, 23% of sign-on awards were make-whole awards for Russell 3000 companies, up from 19% in 2024. The increase was more significant for S&P 500 companies, with 53% of sign-on awards citing make-whole considerations, a substantial increase from 39% the previous year (45% in 2023).

While many companies regard make-whole awards as a necessary tool to entice executives to leave their existing employer, the use of such awards may also result in significantly increased sign-on costs. Sign-on make-whole awards for S&P 500 companies averaged approximately $4.6 million, compared to an average value of $3.5 million for all sign-on awards granted by S&P 500 companies. As a result, 70% of the value of all sign-on awards was intended, at least in part, to compensate employees for amounts forfeited from a prior employer.

Moreover, companies have also increased their use of retention awards to induce current employees not to leave. Among S&P 500 companies, we observed a 61% increase in the number of retention awards granted, while the average value of these awards shot up from $2.4 million to $3.9 million.

Such grants are likely intended, at least in part, to make it more expensive for other employers to poach executives – but run the risk of creating a feedback loop. Increases in the prevalence and value of retention awards can lead to further increases in the use of make-whole awards, which in turn lead back to further increases in retention awards.

Ultimately, the result is a substantial increase in the cost of executive transitions and pay in general. This cycle of rising costs can have significant implications for the succession planning process, and places additional responsibility on the board to explain its decisions and demonstrate that the awards are in the company’s interest.

Market Views and Responses to Our Policy Survey

Arguably, make-whole grants are less contentious than brand new recruitment awards because they make up for amounts being forfeited. Nonetheless, they have the potential to increase the cost of external hires considerably.

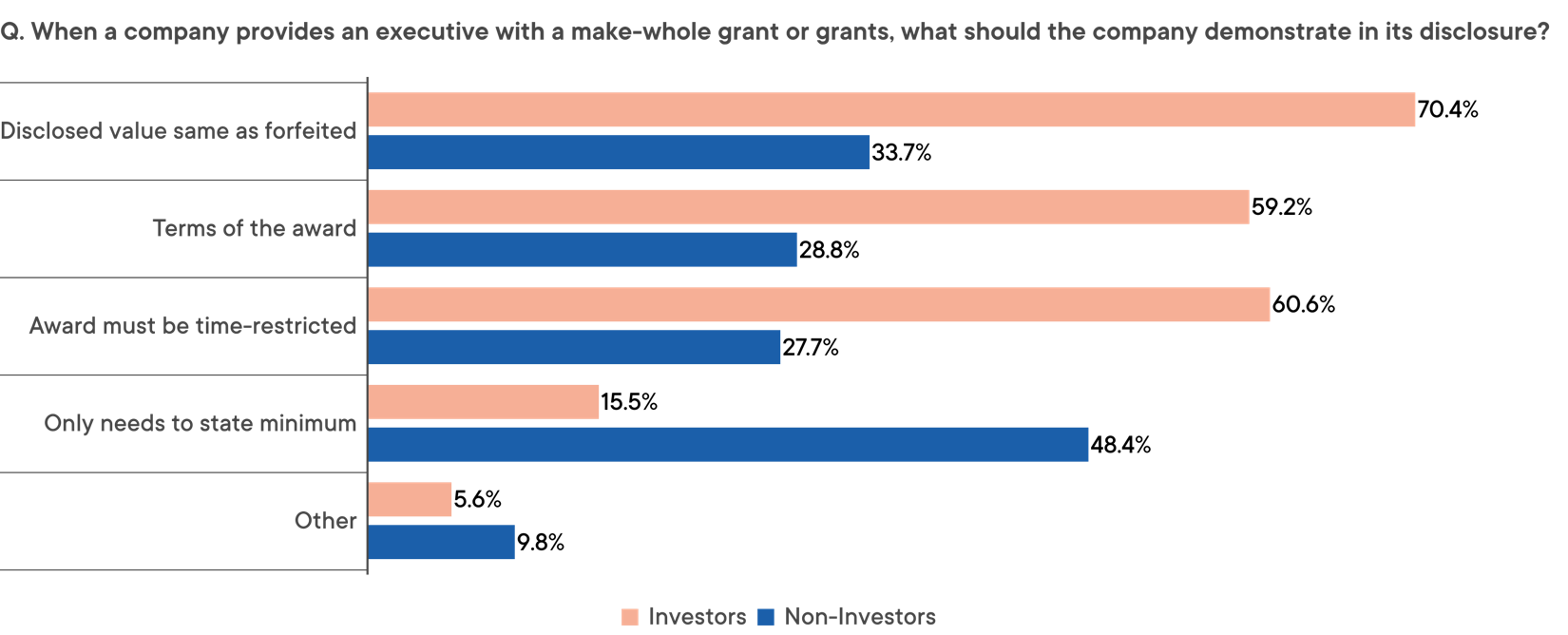

In our 2024 Policy Survey, we asked about disclosure expectations for these awards, and found a significant gap in investor and non-investor7 views (Figure 4). On average, 63.4% of investors expect disclosure of the terms of the award, along with explicit confirmation that awards are time-restricted and the same size as those forfeited, vs. 30.1% among non-investors. By contrast, nearly half of non-investors responded that companies should only need to provide minimum disclosure (48.4% vs. 15.5% of investors).8

Figure 4. Survey Response Regarding Expectations for Make-Whole Grant Disclosure

Source: 2024 Glass Lewis Policy Survey.

One U.S. investor stated:

“We would prefer a detailed breakdown, but often that is not made available. …[W]e will try to reconcile the terms and value of the award with any previous public disclosures made at the executive’s prior employer. Failing that, we will generally take the company at their word, but would engage if we hold a material position.”

Comments left by U.S. non-investors indicate a reluctance to adopt general rules for disclosure, instead favoring board discretion:

“We use guidelines, but if it is material enough as compared to prior or other similar employee grants, then a fuller explanation is warranted.”

“If a company feels a make whole payment is necessary and that it might raise investor questions, they should disclose what will help explain that decision. Why would we apply a general rule here?”

“In the best case … investors should simply agree that the company had all the elements to make the best decisions, and no reason to waste money.”9

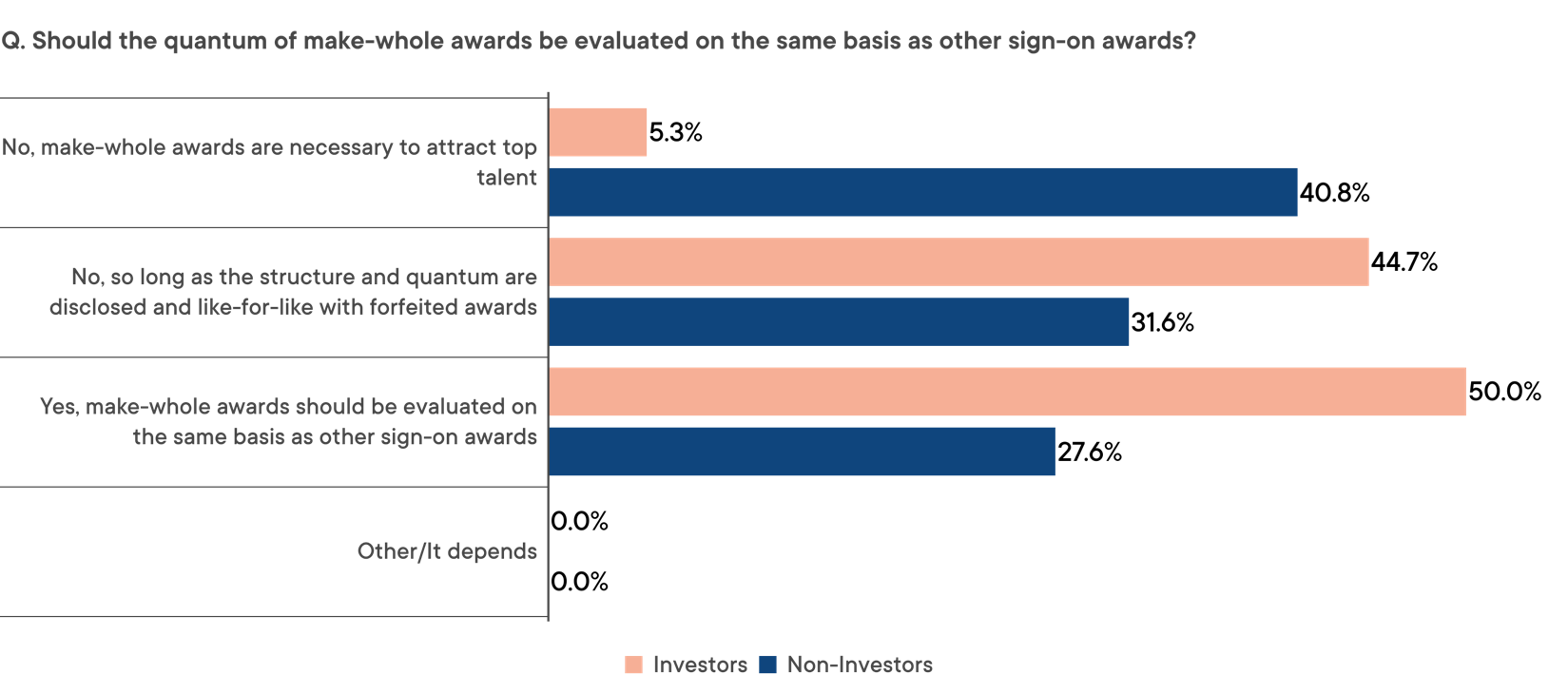

Since then, use of the make-whole designation for sign-on awards has risen, as discussed above. In light of this trend and evident disparity in expectations, we followed up on our 2025 policy survey to better understand market perspectives on how make-whole awards are assessed – and in particular, if they are subject to the same level of scrutiny as other sign-on awards.

Non-investors were far more likely to view make whole awards as fundamentally different from other sign-on awards (Figure 4). Investors were split. While the top answer was to treat make-whole grants on the same basis as other sign on awards, nearly as many were willing to view them differently so long as the grants are fully disclosed and clearly equivalent to what was forfeited.10

Figure 4. Survey Response to How Make-Whole Awards Should Be Assessed

Source: 2025 Glass Lewis Policy Survey.

Conclusion

Make-whole awards have become a common component of executive hiring. At the same time, the sharp increase in both the prevalence and value of retention awards suggests that boards are responding to heightened competition for executive talent by relying more heavily on one-off compensation tools, especially in periods of leadership transition and external recruitment.

Looking ahead, these dynamics suggest that elevated sign-on and retention award values may persist into the 2026 proxy season, particularly if executive mobility remains high and companies continue to compete aggressively for external candidates. As these practices become more entrenched, the importance of robust disclosure and careful calibration of one-time awards will only increase.

Notes and References

1 Boyle, Matthew. “The True Cost of Firing a CEO”. Bloomberg. August 19, 2025. Accessed February 13, 2026. https://www.bloomberg.com/features/2025-cost-firing-ceo/

2 Glass Lewis. 2025 U.S. Market Snapshot.

3 Glass Lewis. 2025 U.S. Proxy Season Review.

4 Ibid.

5 Ibid.

6 Named executive officers are typically the CEO, CFO, and a company’s other three most highly compensated executive officers serving as of the last completed fiscal year.

7 "Non-investor" represents all survey respondents who did not identify as investors, including corporate issuers, representative bodies, consultants, law firms, NGOs and other stakeholders.

8 Glass Lewis. 2024 Policy Survey.

9 Ibid.

10 Glass Lewis. 2025 Policy Survey.

.jpg)

.png)