Key Takeaways

In the third installment of our Proxy Season Global Briefing, we provide a rundown of headlines and key trends relating to director elections and board composition from around the globe. Glass Lewis clients can also access the full report via the content libraries on Viewpoint and Governance Hub. For more proxy season trends, read part one and part two of this ongoing four-part series.

The board of directors is at the heart of corporate governance – and at the heart of ongoing debate around the basis for selecting directors, and what they should be tasked with overseeing.

Shareholder Vote Results: Director Elections and Opposition

Shareholder voting on board elections remained largely consistent in North America.

- In our overall U.S. coverage, 72 director nominees failed to receive majority support (versus 69 last year, down from 93 in 2023). Director elections in the Russell 3000 index also remained largely consistent, with 33 failed director elections in 2025 compared to 39 in 2024.

- Of these 72, only nine have left their boards thus far and three directors’ resignations have been rejected. The prevalence of plurality voting standards and resignation policies in the U.S. means that, generally, relatively few directors depart their boards after failing to receive majority support.

- In Canada, 10 director nominees failed to receive majority support, continuing an upward trend (compared to nine in 2024, seven in 2023 and three in 2022).

- Seven of these failed directors were concentrated to two boards: four at a TSX Venture Exchange-listed pharmaceuticals company and three at a TSX-listed mineral exploration company.

Shareholder dissent on director elections at large European companies remains minimal.

- No blue chip uncontested director elections failed, and dissent over 20% was only seen at 2% of companies. Belgium and France had the highest number of contentious proposals (nine and eight, respectively).

- The closest call was seen in French hospitality company Accor SA, where former French president Nicolas Sarkozy, currently serving house arrest for corruption, was re-elected with 52% support.

- At Ferrexpo, a Swiss-based, UK FTSE All-Share-listed company, director Vitalii Lisovenko did not receive majority support from independent shareholders for the second consecutive year. Under UK Listing Rules, Lisovenko remains on the board pending an additional vote by all shareholders.

Director opposition declined in Australia, but remains high by historical standards.

- 17 board-endorsed directors received over 25% dissent in the most recent proxy season, – down from 25 the year before, but still higher than the historical range of 10-15. Dissent was driven by familiar issues: disappointing share performance, operational challenges, capital allocation and concerns over board composition. In several cases, lack of board diversity was a factor, though never as a standalone issue.

- There was a clear overlap between companies receiving remuneration strikes and those facing director dissent. In some cases, directors faced significant remuneration-related opposition even without a strike.

Gender Diversity on Boards

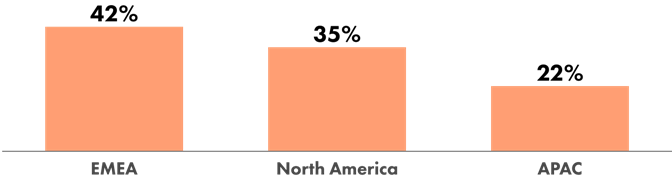

Board gender diversity continues to increase across Europe, Middle East and Africa (EMEA); North America and Asia-Pacific (APAC), but remains lower in leadership and executive positions.

Figure 1. Average Board Gender Diversity at Large Cap Companies in EMEA, North America and Asia-Pacific

Source: Glass Lewis

- A majority of European blue chip index constituents have board gender diverse representation over 40%. Belgium and Switzerland lag, with less than half of boards featuring gender diverse representation over 40%.

- Executive gender diversity levels were consistent year-on-year, but significant variation remains from country to country. At least one blue chip company in each of Denmark, Italy, the Netherlands, Sweden, Switzerland and the UK has no gender diverse executive.

- Gender diversity on North American boards and key committees increased slightly compared to last year, remaining around 30% in the U.S. Russell 3000 and around 40% in Canada’s S&P/TSX Composite.

- While board diversity increases in Asia-Pacific were generally modest, there has been a substantial reduction in the number of boards with no gender diverse directors.

- In Japan, the number of Prime-listed boards with no gender diverse directors decreased from 4.9% to 2.8%. Nearly one-third of TOPIX 100 boards had at least 30% gender diversity.

- In Korea, the overall proportion of gender diverse directors increased marginally from 8.2% in 2024 to 9% in 2025, while the proportion of gender diverse executives remained static at 5.3%.

- Although large Korean companies are required to appoint a minimum of one gender diverse director, there are no penalties for non-compliance, and 5.6% of large company boards include no gender diverse directors.

- In Hong Kong, the average proportion of board gender diversity for companies in the Hang Seng Large Cap Index reached 21.1% (compared to 20% in 2024, 19% in 2023 and 17% in 2022: 17%).

- Board gender diversity levels continue to vary significantly across and within Latin America markets.

- Despite the introduction of ‘comply-or-explain’ recommendations on board diversity in Brazil, boards with no gender diverse directors still remain common practice in the market.

Board Diversity Beyond Gender

Board racial/ethnic diversity continues to increase among North American and UK companies, but we observed a drop in U.S. companies providing aggregate or individual director demographic information.

- Many U.S. companies significantly revised their disclosures of board diversity in 2025. While reporting remains widespread, the percentage of Russell 1000 companies that disclosed the racial/ethnic diversity of directors on either the aggregate board or individual director level declined from 94.1% last year to ~70%.

- Among companies that provided this disclosure, board racial/ethnic diversity levels increased slightly for both the S&P 500 (26.3% in 2025, up from 25.3% in 2024 and 23.4% in 2023) and Russell 1000 (24.8% in 2025, up from 24% in 2024 and 22.1% in 2023).

- In Canada, 86% of S&P/TSX 60 (versus 88% in 2024) companies provided clear disclosure regarding racial/ethnic diversity on the board. Of these companies, average board racial/ethnic diversity was 16.6% (compared to 16.9% in 2024).

- Just 15 Canadian companies had a board that was at least 20% racially/ethnically diverse.

- In the United Kingdom, 92% of FTSE 350 companies (with 87% in 2024) and 98% of FTSE 100 companies have achieved the Parker Review target of at least one ethnic minority director on the board.

- Where ethnicities are disclosed, ethnic minority directors represent on average 17% of the board in the FTSE 350 index.

Looking for More?

Check our blog for additional instalments of our Proxy Season Global Briefing. Glass Lewis clients can also access the full report via the content libraries on Viewpoint and Governance Hub. We will also share more of our proxy season findings, including details of Glass Lewis voting recommendations and analysis, via a series of market-specific Proxy Season Reviews in September and webinars in October.