Key Takeaways

The Raise in Repeated Strikes

In 2023, the Australian market witnessed a surge in shareholder opposition to executive pay. A record-breaking 41 remuneration strikes raised questions about whether this marked a temporary spike or the onset of a lasting trend. The 2024 data suggests that shareholder dissent—especially on executive pay—remains elevated.

There were 40 remuneration report strikes in the ASX300 in 2024, the second-highest total since the two-strike rule came into force. This marks a notable jump from the typical range of 22–26 in previous years.

ASX 300 Remuneration Report Strikes (25%+ Against)

The most striking development was the increase in repeat offenders. Thirteen companies received consecutive strikes, up from just five in each of the two previous years. NRW Holdings topped the list with its seventh consecutive strike. Lovisa Holdings and Dicker Data each hit four in a row, and ten others received their second.

Proportion of Repeated Remuneration Strikes in ASX 300

This trend points to a persistent disconnect between boards and their investors. Some boards are clearly struggling to meaningfully address shareholder concerns. Others may be choosing to weather the dissent, perhaps valuing executive retention or stability more than avoiding a strike.

Analyzing companies repeatedly facing shareholder strikes reveals some noteworthy patterns. Six of the 13 companies have influential figures such as founders or major shareholders on the board. Additionally, two companies feature long-standing CEO-chair relationships, indicating a strong, well-established dynamic that may reduce responsiveness to shareholder concerns. These relationships can make it more difficult for boards to challenge executive decisions or pivot based on investor feedback.

Two consecutive remuneration strikes results in a “board spill” proposal, with all directors required to stand for re-election. However, despite the dissatisfaction, shareholder frustration rarely extends beyond advisory votes. Board spill resolutions remained largely symbolic in 2024, averaging under 7% support. Additionally, every board-endorsed director within the ASX300 ultimately secured re-election in 2024. This suggests that while investors are voicing disapproval on remuneration, the concerns aren’t spilling over into other voting items—potentially making some boards less responsive to broader shareholder feedback.

Intensity and Themes Behind the Remuneration Strikes

In terms of voting intensity, many remuneration strikes in 2024 clustered in the lower opposition range of 25%–35%, contributing to a modest decline in the average level of dissent—from 46% in 2023 to 42% in 2024.

Still, several companies saw intense pushback. Perpetual recorded the highest level of dissent, with 88% of shareholders voting against the remuneration report. The backlash followed declining share prices and discontent over M&A strategy, making retention bonuses and incentive payouts particularly contentious. Mineral Resources followed with 75% opposition, amid ongoing scrutiny of founder Chris Ellison.

Strikes by Against Vote

Common drivers of shareholder dissent include perceptions of preferential executive treatment, inappropriate incentive payouts and retention awards. Interestingly, discretionary uplifts in incentive outcomes—once a common flashpoint—were not a major issue in 2024. Boards may have learned that applying upward discretion often almost guarantees a strike.

Other recurring issues included base pay increases, reliance on short-term incentives and a perceived lack of 'skin in the game.' Additionally, scrutiny of long-term incentive (LTI) targets grew. Investors increasingly expect these targets to reflect external realities such as market conditions and analyst forecasts.

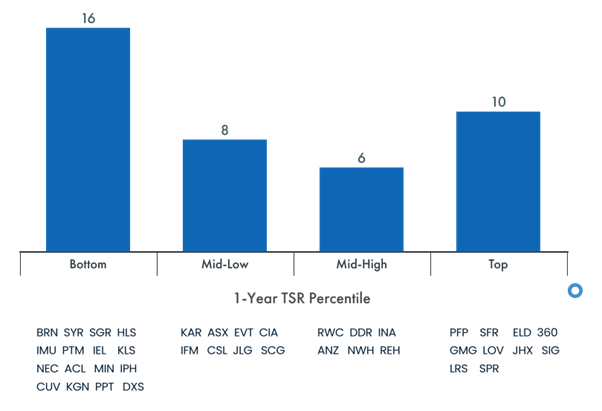

Dissent was closely tied to weak shareholder returns. An analysis of relative total shareholder return (TSR) shows companies in the bottom quartile were much more likely to receive a strike, confirming a strong link between poor performance and dissent.

ASX 300 Strikes by 1-Year Relative TSR

Director Elections and Underlying Concerns

While all board-nominated directors were re-elected, shareholder dissent did extend beyond remuneration, with some director elections also drawing scrutiny. Seventeen board-endorsed directors received over 25% against votes in 2024—down from 25 the year before, but still higher than the historical range of 10–15.

The dissent was driven by familiar issues: disappointing share performance, operational challenges, capital allocation and concerns over board composition. In several cases, lack of board diversity featured in the mix, though never as a standalone issue.

There was a clear overlap between companies receiving remuneration strikes and those facing director dissent. In some cases, directors faced significant remuneration-related opposition even without a formal strike, underscoring the link between executive pay and board accountability.

Non-board-endorsed candidates again failed to gain traction, with four nominations and zero majority wins.

ASX 300 Opposition Against Directors (25%+ Against)

Trends in E&S Shareholder Proposals & Climate Transition Plan Votes

A total of 15 environmental and social (E&S) shareholder proposals were submitted across six ASX300 companies in 2024. This continues a gradual decline observed in recent years, partly due to the emergence of alternative engagement mechanisms.

Management-sponsored climate plan votes (aka Say on Climate) have become increasingly common since 2021. These proposals are voluntary and non-binding. Member statements, introduced more recently, also give shareholders a platform to advocate over climate-related concerns—most often by recommending votes against the election of directors, remuneration reports and climate plans. In 2024, member statements were included in notices of meeting at Woodside Energy Group, Santos, and Whitehaven Coal.

Climate remained a dominant theme among E&S shareholder proposals in 2024. APA Group faced a capital allocation proposal, while three of the four major banks—Westpac, NAB, and ANZ—received climate-related resolutions.

A notable development in 2024 was the increased focus on biodiversity. Australia's two largest grocery retailers, Woolworths Group and Coles Group, were targeted by the Sustainable Investment Exchange (SIX) over their sourcing of farmed salmon from Tasmania’s Macquarie Harbour—a region home to the endangered Maugean skate. Proposals calling for increased disclosure received relatively strong support—over 30% at Woolworths and 40% at Coles. However, calls to stop sourcing salmon entirely were far less popular, receiving only 5% and 7% support, respectively. This highlights a consistent pattern: disclosure-based proposals tend to receive significantly more shareholder support than those calling for direct operational changes.

Two Say on Climate votes were held in 2024. Woodside’s proposal received the highest global level of opposition to date, with support falling below 50%—marking the first time that any company, globally, has failed a Say on Climate vote. In contrast, BHP’s climate plan received strong support, passing with more than 90%. Looking to 2025, several companies are expected to hold follow-up votes as part of a triennial commitment.

This post draws from data collected by CGI Glass Lewis during the 2024 proxy season in Australia, which was presented at the 19th Annual Remuneration & Governance Forum, co-hosted by CGI Glass Lewis and Guerdon Associates in March 2025. You can read summaries of what was discussed at the Forum in separate articles covering remuneration and governance.